immi, a healthy ramen company that Pear first backed in their pre-seed round, has been experiencing rapid brand growth lately. But while a few of their marketing successes have been a result of good luck (like Usher’s talent agency reaching out after seeing an immi-branded truck in NYC), most of their success stems from their experimental approach to marketing.

The immi team understands that there is no silver bullet when it comes to brand building, and there is no rule book on creating a halo effect, particularly when it comes to growing an organic social audience. Nevertheless, the team at immi has cultivated brand loyalty and tremendous growth in the last two years.

I sat down to chat with immi’s co-founder (and fun fact: former Pear team member!) Kevin Lee about how immi grew an audience for healthy ramen from scratch — and in the early days, with zero marketing budget.

Here are the key takeaways in Kevin’s own words (this post has been edited for brevity):

In the early days, you have to do things that don’t scale.

During the R&D phase, we found a bot online that would scrape all of Reddit and send a Slack notification when certain keywords were mentioned. We indexed for keywords like “low carb ramen”, “healthy ramen”, “instant ramen alternatives”, etc. I was looking at these comments and posts seven days a week, figuring out a smart way to insert ourselves into the conversation.

There was no product yet, just a Shopify landing page. But with a well-placed, thoughtful comment, you could drive 500 email signups with one comment. Like any startup, we were trying to acquire email leads as cost-efficiently and quickly as possible without a marketing budget. We also used some Meta ad credits to test some paid lead ad forms on Meta, which I’d say generated much higher quality leads four years ago than they do today.

We got benchmark data to estimate the avg. open rate, click through rate, AOV, and conversion for a waitlist email subscriber and were able to back into the cost per lead for an e-mail in order to break even on our launch.

Once we figured out that figure, we started scaling our organic and paid efforts to acquire emails.

Once someone got on our email list, we had an email flow that we wanted to feel super authentic. We used gifs of ourselves goofing off in the kitchen… things that reminded customers that we’re a homegrown upstart brand. We also made a private Facebook community where we shared the behind-the-scenes of building the company and gradually turned members into loyal immi evangelists. It was important to us to build a loyal, thriving community from the start and we knew higher engagement would result in higher conversion rates.

Our thesis panned almost exactly to the tee and in our first month of launch, we generated multiple six figures of revenue from our e-mail waitlist without spending any marketing dollars.

Gif from the immi email flow

Approach your marketing like a product manager would.

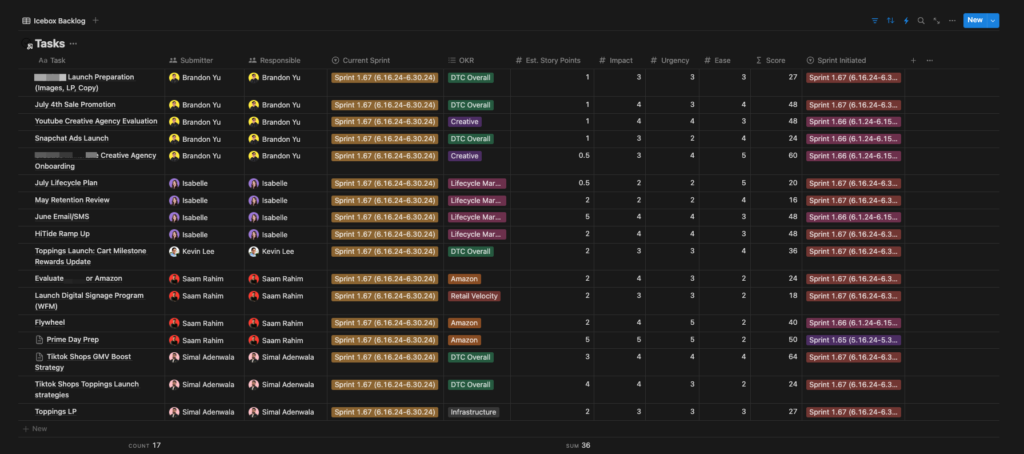

My co-founder and I worked as PMs in tech for the past decade, so we naturally applied the PM framework to marketing: creating a marketing icebox and running sprint planning. The icebox is a backlog of growth ideas that anyone in the org can add to. You have to add context and prioritization from the lens of three variables: impact, urgency, and ease. You have story points, which is an estimate of how many days it will take to actually accomplish this task.

A marketing sprint planning session

We do sprint planning two times a month. We’ll review the top priority ideas and each person will then assign themselves to sprint items. At the end of the sprint, we run a retrospective to report on results of each experiment and plan for the next sprint. Standard product management stuff.

The immi team experimented with a lot of ideas, like handing out ramen from a branded truck in Times Square

Run your marketing like a writers room.

We run additional creative sprints that everyone across the immi team is welcome to join. Each person has to come up with 3-5 novel or unique ad concepts and they’re responsible for scripting out the ad copy and video / image scenes.

We also created a writers room inspired by comedy and TV series writers who work on short deadlines. We pick themes for each writer’s room i.e. Mothers Day, ideas are thrown out rapidly and just as quickly shut down. You can’t criticize the person, only the idea because you don’t want people to clam up over time. When people like an idea, we jot it down, expand on it, iterate on dozens of variations until we agree on the final concept, and then we test it out. We do this every other week.

Organic media success is impossible to quantify, but there’s power in iteration and experimentation.

One idea that spun out of our writers room is a TikTok series called Ramen on the Street. Our in-house TikTok strategist dresses in an immi ramen packet costume and roams around NYC interviewing people with deep life questions to draw out answers that make you feel good as a viewer. The overarching idea was based on our internal tagline at immi: ramen that makes you feel good. A good brand moves beyond selling a product to selling a feeling (and ultimately, an identity). We want people to feel good from our content and associate that feeling with our product.

It took us nine months to iterate into a repeatable series. Nine months of zero traction and zero engagement was tough for the team. It was like running another startup within the startup. But as long as you’re iterating on your learnings and running experiments, you’re probably going to find some repeatable angle over time.

An example of our TikTok team’s experiment was quite literally rubbing a light layer of Vaseline on the camera lens. It creates a blur effect that makes the video feel a little bit more organic, and believe it or not, that was one of the catalysts to our videos taking off.

An immi creator in a ramen costume

As a founder, you have to find the balance between stubbornness vs. grit. I’m not going to say we weren’t lucky, but I do believe our team did a great job of constantly experimenting and iterating until we found success.

Now we’re consistently doing 10-20 million organic views per month, and we’re also able to iterate on that content. We’re trying CTA’s at the end of videos to drive people into retail stores. We’re also starting to test content where we’re interviewing people in the ramen aisle of grocery stores where immi is visible.

Over time, you really want to build a media platform that is driving organic traffic to you instead of spending all your money on paid ads. There’s magic in this type of marketing. It’s hard to quantify the magic, because when you quantify the magic, the magic disappears. We’re very data oriented, don’t get me wrong, but I think these are the exceptions you have to make.

Focus on one thing at a time. When it reaches saturation, expand.

Through the lifespan of immi, we’ve always tried to focus on one thing at a time. First, it was driving people into our email flow. Then we focused on making Meta ads work. No shiny object syndrome. We pick one, get early signs of channel market fit, and triple down. Many founders try to spread themselves across 10 different channels when the reality is that you only need one at a time to really scale up until you hit a breaking point. When you hit saturation, broaden to a new channel.

Immi team serving ramen to trade show attendees

Thank you to Kevin for sharing these insights! To learn more about immi please visit them online or follow them on TikTok. You can find immi in Whole Foods, Target, Sprouts, HEB, GNC, and more.

immi’s media machine has helped them get interest (and investment) from celebrities like Usher, Kygo, Apolo Ohno, Naomi Osaka, a TikTok duet from Lizzo, a partnership for Disney/Pixar’s Inside Out 2 and more. For more founder learnings, check out the Pear Almanac.

Earlier this week, PearX S19 alum Learn to Win (L2W) announced a $30M Series A round, led by the Westly Group and joined by Pear and Norwest Venture Partners. L2W’s software improves training & onboarding for a wide range of enterprise clients, from the Los Angeles Rams to the U.S. Air Force. They do this better than anyone else by using data analytics and AI to personalize learning effectiveness for their customers.

We first backed L2W in 2019, and now five years later, we are honored to double down our support for them. To mark the occasion, we wanted to reflect on our partnership with L2W and the amazing progress they’ve made over the last five years.

We met the founders of L2W, Sasha Seymore and Andrew Powell, in 2019 when they were students at Stanford GSB. We met as part of a business plan competition and our teams hit it off. They’d been chewing over the concept behind L2W for years, but they finally got it off the ground in 2018 while at the GSB.

Sasha & Andrew at Stanford GSB

We met them when they were just two co-founders and an idea with a little traction, and we decided to back them for a few major reasons:

First, the founding team was fully dedicated to pursuing the idea: Sasha and Andrew met their freshmen year as Morehead-Cain scholars at the University of North Carolina at Chapel Hill, and they were roommates throughout undergrad. They started discussing the concept of L2W during that time. Following graduation, they went their separate ways: Andrew to Mauritius and Sasha to play basketball in Europe. Although they were apart for three years, they continued to discuss the company and what it could be. And then completely by coincidence, they were both accepted into Stanford GSB at the same time and decided to room together once again. It felt like fate, so they were drawn to pursue L2W officially.

Founders while students at UNC

Second, they solved a problem that they were passionate about: Andrew was really interested in education and had spent three years at The African Leadership University in Mauritius designing new learning models. Sasha was a basketball player at the University of North Carolina at Chapel Hill, had spent time studying the possibilities of peace through sports.They combined their passions in education and sports to create a new method for training athletes. Their initial pitch to us was: Learn to Win is a “Rosetta Stone” of playbook learning, turning playbook and gameplan materials into an interactive learning experience and providing coaches insight and analytics into what their players understand and what they do not.

Lastly, they knew the market was huge. While they started by focusing primarily on sports teams, they knew that there were many zero tolerance environments and industries used training tools that don’t match the demands they face. The L2W team had a vision to expand to industries like the military, aviation, and oil and gas.

L2W pitch deck in 2019

They applied and were accepted into PearX’s Summer 2019 cohort. At the time, they knew they had a big opportunity in front of them, and they’d gained some early traction with a few clients.They wanted to use their PearX experience to really hit the gas and accelerate their company forward. Through the 14 week PearX cohort, they onboarded many new customers to their microlearning modules, and by the time Demo Day rolled around, they had 100+ clients and over $1M in sales. They also expanded beyond sports during PearX and signed a large contract with the U.S. Air Force.

2019 PearX Demo Day pitch

PearX S19 cohort, which included companies like Windborne, Polimorphic, Learn to Win, Xilis, and Gradio.

Following Demo Day, they raised a $4M seed round in 2020 led by Norwest Venture Partners and joined by Pear and 20|20 Fund. They continued working out of Pear’s offices in Palo Alto for a period of time, so we had the chance to work side by side with the team and see their progress. Over the following few years, they grew from a team of 2 into a full-time staff of 30+. They continued to refine and evolve their product, and onboarded hundreds of enterprise clients like Chick-fil-A, the U.S. Department of Defense, and professional sports teams like the Carolina Panthers. In the last few years, they’ve expanded and refined their platform, involving even more learning science and AI to better help customers with their training.

With this latest $30M Series A fundraise, we know they’ll be able to take it even further. Their path has been exciting to witness and we are excited to see where they take the tool next.

Here at Pear, we specialize in backing companies at the pre-seed and seed stages, and we work closely with our founders to bring their breakthrough ideas, technologies, and businesses from 0 to 1. Because we are passionate about the journey from bench to business, we created this series to share stories from leaders in biotech and academia and to highlight the real-world impact of emerging life sciences research and technologies. Read more about Pear’s approach in biotech here.

In this review, we look back at the top 50 biotech companies of the past 15 years. This post was written by Pear Partner Eddie and Pear PhD Fellows Alan Tung, Ami Thakrar, and Gary Li.

Introduction:

Life sciences companies have the unique opportunity to transform scientific discoveries into drugs, diagnostics, and technologies that can substantially improve people’s well being. In the past decade and a half, we’ve seen dramatic progress in the sector: the approval of several highly impactful drugs (e.g., COVID vaccines, checkpoint inhibitors, GLP-1 agonists), the rapid maturation of emerging therapeutic modalities (gene therapies, cell therapies, gene editing, protein degraders, ADCs, radiopharma, etc.), and the increasing adoption of technologies used in biology research and in diagnostics (NGS, epigenetics, transcriptomics, proteomics, single cell biology, spatial biology, organoids, etc.).

We were motivated to highlight 50 biotech startups that have recently generated tremendous value for patients, for investors, and for the sector. Given the long development timelines involved in biotech, we focused this review on companies founded within the past 15 years, and we limited the scope to life sciences startups developing therapeutics, diagnostics, or tools.

As an admittedly imperfect indicator for the value generated, the top 50 startups were selected and ranked based on the valuations actually realized during the period via an exit by acquisition or a public financing. For the companies that went public and remained independent, we looked at the maximum of either the market cap at IPO or the market cap achieved at the end of the period.

To get a better sense of what these companies look like, we surveyed these “biotech behemoths” below with respect to their key products, the profiles of the founding CEOs and scientific founders, the origins of their lead programs and technologies, the founding location, the time to an initial exit, and several other characteristics of interest.

Methods:

Using Pitchbook, we screened for therapeutics, diagnostics, and life sciences tools companies founded between Jan 1, 2009 – Dec 31, 2023 in the US, Canada, and Europe. The top 50 companies were selected based upon the maximum of: the upfront or guaranteed value realized at the time of acquisition, or the company market capitalization either at IPO or at the end of the period on Dec. 31, 2023.

This approach means that a few companies were included that had a very high valuation at IPO, but ultimately did not retain this value (e.g., because of a subsequent disappointing clinical trial outcome). Given that different investors have different strategies when it comes to unwinding their positions in public companies, our intent in using this particular criterion was to prioritize those companies throughout the period that were likely to have been most meaningful in terms of financial value returned back to investors.

Spinouts from major companies were generally excluded; notable exclusions include Cerevel Therapeutics, spun out of Pfizer in 2018 and acquired by AbbVie in 2023 for $8.7B, and Viela Bio, spun out of AstraZeneca also in 2018 and bought by Horizon for $3B in 2021. However, we decided to include Grail, spun out of Illumina to work on a product application quite distinct from Illumina’s main NGS tool platform, as well as Telavant and Immunovant, spinouts of Roivant – which is itself a startup.

A handful of companies were identified and added to the list based on cross referencing Crunchbase, Pitchbook’s public company screener, and relevant biotech industry news sources and reports. Additional data pertaining to company and founder characteristics were obtained from company websites, press releases, SEC filings, available news sources, or where possible, primary research.

Constraints:

1) The valuation metric we applied for ranking is neither an intrinsic measure of value nor impact.

2) Many companies that ultimately generate tremendous benefits for patients or the industry get acquired or exit at an earlier stage at a lower value.

3) As noted above, some companies included in this ranking that were highly valued at the time of IPO or acquisition did not live up to this valuation due to clinical setbacks or commercial challenges.

4) We exclusively focused on the outliers in terms of success, and we did not run a comparison against companies that were not as successful. Accordingly, we would caution against any tendencies to form conclusions that suffer from survivorship bias.

5) Our data and results are limited by the available resources that we had access to as noted above. (Note: if we made any omissions or errors, please kindly let us know!)

6) The valuations were not adjusted for inflation.

Pear VC’s Biotech Behemoth rankings:

Product Impact

Among the behemoths, a whopping 46 (92%) were therapeutics companies, 3 (6%) were diagnostics companies, and 1 (2%) was a life sciences tools company. In the sections below, we survey some of their key products.

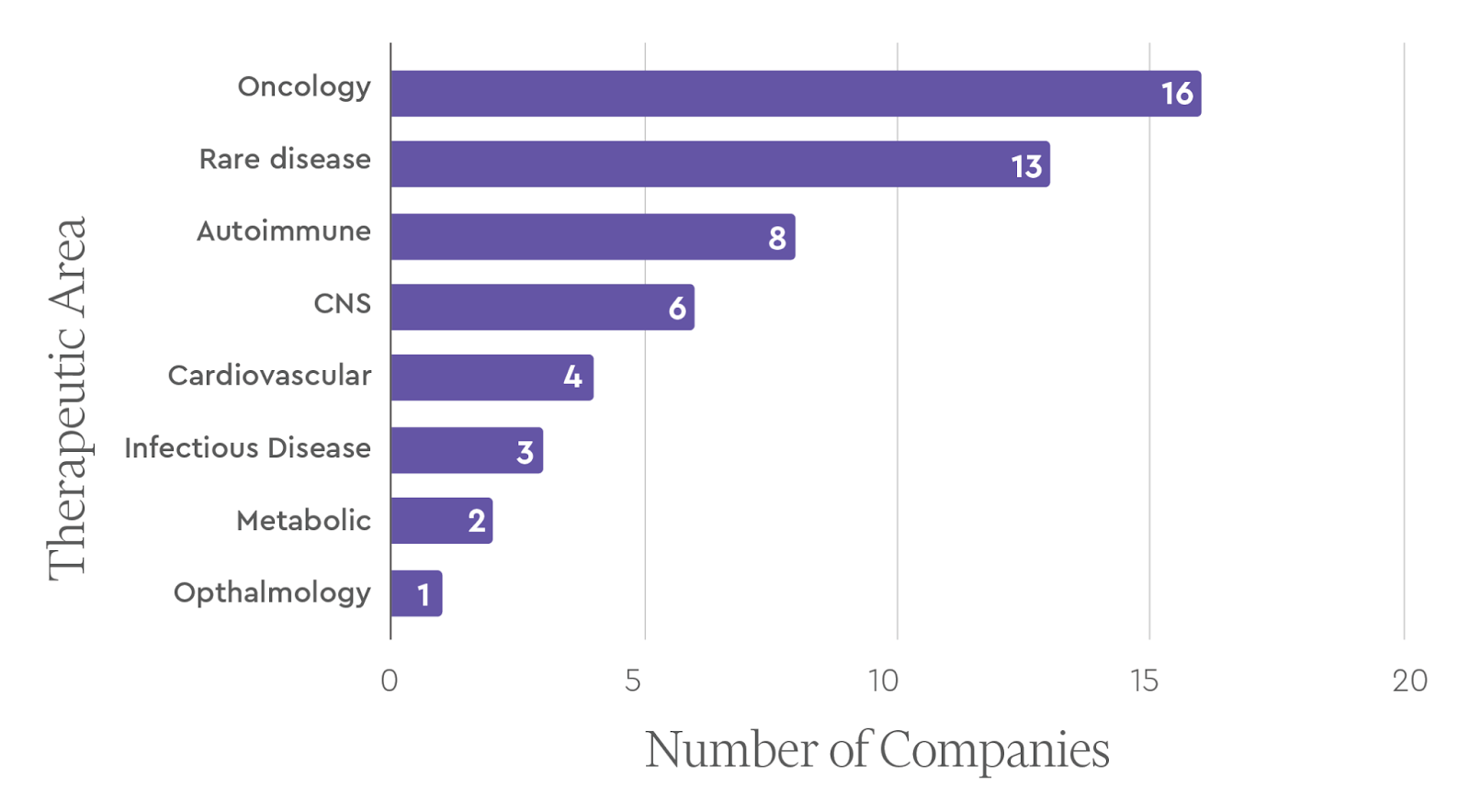

Therapeutics Companies – Indication Focus

The 46 therapeutics behemoths spanned all of the major indication areas including oncology, immunology, CNS diseases, and infectious diseases. Oncology was the most common lead therapeutic area (16 companies, 34.78%), followed by rare diseases (13 companies, 28.26%).

Current Clinical Stage of Therapeutics Behemoths (EOY 2023)

Among the top therapeutics companies, a majority (52%) achieved FDA approval for their lead drug programs by the end of 2023, with about a quarter reaching Phase 3 and the remainder in earlier clinical stages.

Snapshot of approved drugs by the top drug companies

We surveyed the approved drugs developed by the top therapeutics startups in our rankings. Company valuation was generally positively correlated with projected peak sales of the corresponding company’s approved drug.

Developer

Brand Name

Generic Name

Projected Peak Sales* ($B)

Therapeutic Area(s)

Commercial Lead

Approval Year(s)

1

Moderna

SpikeVax

Moderna COVID Vaccine

18.4B (2022)

Infectious Disease

Moderna

2020

2

MyoKardia

Camyzos

Mavacamten

2.3B (2030)

Cardiovascular

BMS

2022

3

Biohaven

Nurtec

Remigepant

2.8B (2030)

CNS

Pfizer

2020

4

Juno

Breyanzi

Lisocabtagene maraleucel

2B (2030)

Oncology

BMS/Celgene

2021

5

Kite

Yescarta

Axicabtagene ciloleucel

2.6B (2029)

Oncology

Gilead

2017

6

Roivant

Vtama

Tapinarof

0.41B (2032)

Autoimmune

Pfizer

2022

7

Avexis

Zolgensma

Onasemnogene abeparvovec-xioi

2.1B (2029)

Rare Disease

Novartis

2019

8

Receptos

Zeposia

Ozanimod

1.7B (2030)

CNS, Autoimmune

BMS

2020

9

Apellis

Empaveli, Syfovre

Pegcetacoplan

0.66 (2029, Empaveli), 2B (2029, Syfovre)

Rare Disease: Ophthalmology

Apellis

2021, 2023

10

Loxo

Vitrakvi, Retevmo

larotrectinib,selpercatinib

0.56 (2028, Vitrakvi), 0.76 (2029, Retevmo)

Oncology

Eli Lilly

2018, 2020

*Source: GlobalData

Platform or asset driven?

Among the top therapeutics companies, there were slightly more platform-driven companies (24 of 46) compared with asset-driven companies (22 of 46), but it is a fairly even split, especially considering that the definition of a platform is subject to a wide degree of interpretation. Here, we defined a platform as a key technology or discovery method that can lead to more than one asset. There are a few major themes among the platform-driven companies including those focused on cell therapies (Juno, Kite, Sana, Lyell, Arcellx); gene therapies (Avexis, Spark, Krystal Biotech, Audentes); CRISPR technology (CRISPR Therapeutics, Intellia); and computationally-driven drug discovery (Nimbus, Recursion).

Dx & Tools Products

There were just four diagnostics or tools companies out of the top 50 companies. Grail (founded in 2018) developed and launched the Galleri test for multi-cancer early detection. 10X Genomics (founded in 2012) commercialized instruments and reagents related to detailed sequencing and characterization of cellular genomes and transcriptomes. Foundation Medicine (founded in 2010) developed multiple tissue-based oncology genetic tests and was acquired by Roche in 2015. Guardant Health (founded in 2012) developed several liquid biopsy-based oncology tests for both early and advanced cancer.

Company

Founded

Key Products

Grail

2015

Galleri blood-based genomic test for early cancer screening

10X Genomics

2012

1. Chromium Single Cell: profile single cell gene expression 2. Visium Spatial: spatial whole transcriptome analysis 3. Xenium In Situ: detecting and imaging RNA

Foundation Medicine

2010

1. FoundationOne CDx: tissue-based companion diagnostic genomic test for solid tumors 2. FoundationOne Liquid CDx: blood-based companion diagnostic genomic test for solid tumors 3. FoundationOne Heme: comprehensive genomic profiling test for hematologic malignancies, sarcoma and certain solid tumors

Guardant Health

2012

1. Guardant360 and Guardant 360CDx: blood-based comprehensive genomic profiling test for therapy selection for solid tumors 2. Reveal: blood-based genomic test for minimal residual disease detection and recurrence monitoring 3. Shield: blood-based genomic test for colorectal cancer screening

Founding profiles:

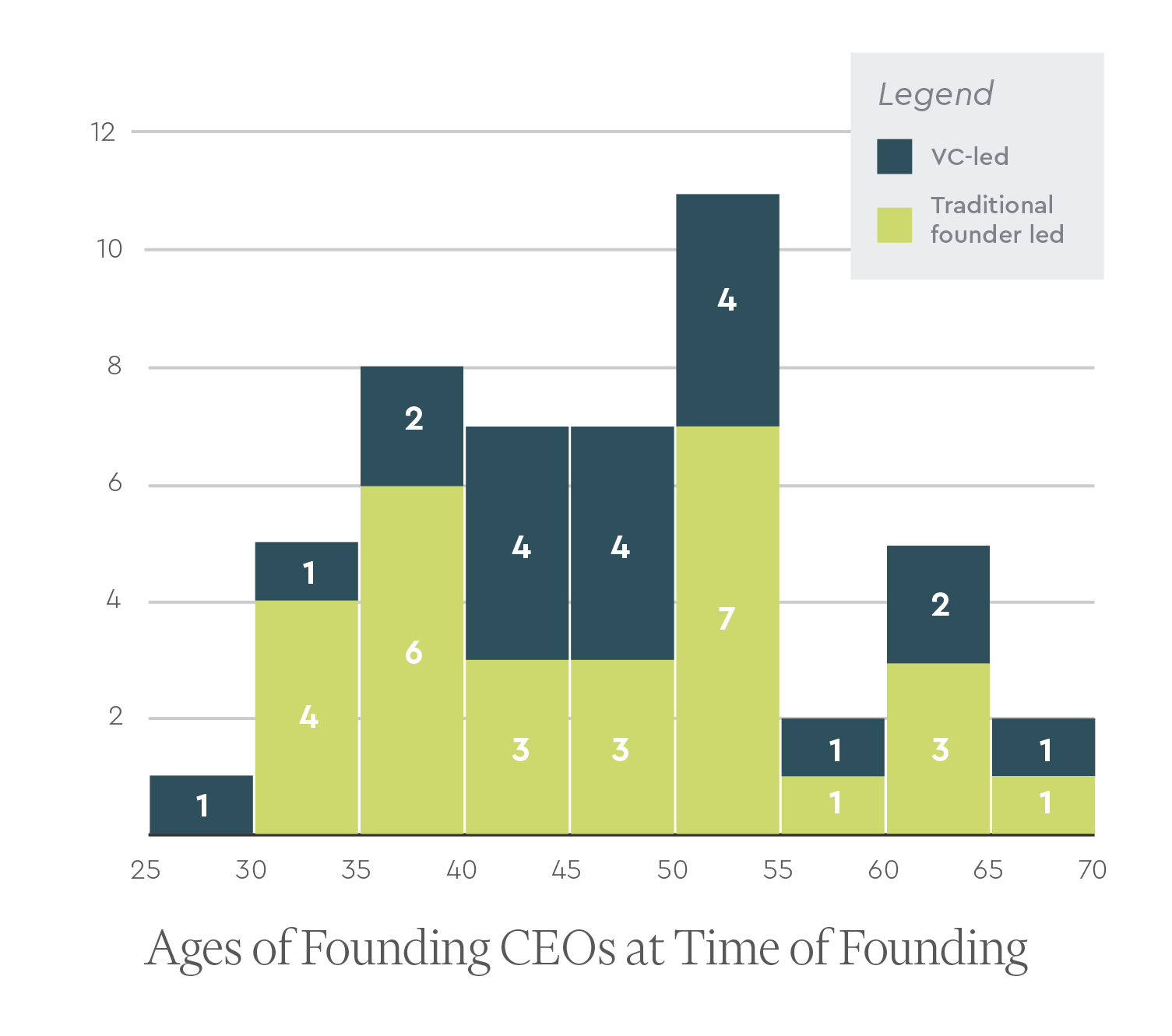

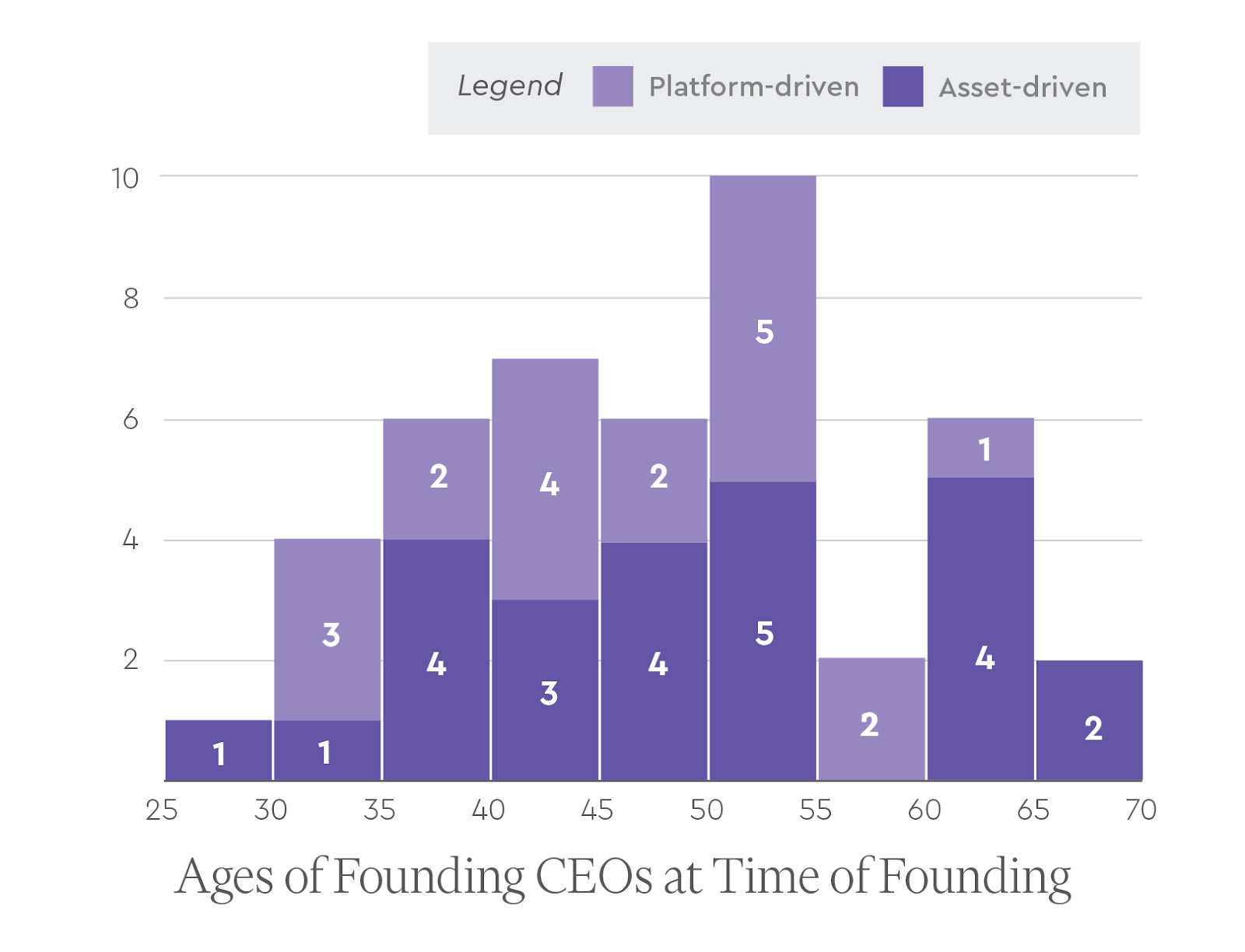

Founding CEO Age

We were able to find data on the age of the founding CEO (+/- 1 year) at the time of founding for 47 of the 50 companies we profiled. We found that across these 47 companies, the average age of the founding CEO at the time of founding was ~46 years old (+/- 10 years). In the diagnostics/tools space (only 4 companies), the average age dropped to 38 (+/- 5 years old), but in therapeutics, the sector that dominates the rankings, the average age was 47 (+/- 10 years old).

We also found no substantial difference in the average age of the CEO at founding for companies that were or were not VC incubated. For companies that were VC-led, the average age of the CEO at founding was ~48 (+/- 10 years old). This is only slightly older than the founding CEOs of companies that were not VC-led, who were on average ~46 years old (+/- 10 years).

We sought to understand if the founding CEO ages were different for platform-driven vs. asset-driven companies. On average, the founding CEOs of platform-driven companies were slightly but not significantly younger at 46 years old (+/- 9 years) compared with those of asset-driven companies at 49 years old (+/- 11 years).

Experienced vs. First-Time CEOs

Interestingly, a little more than half (~53%) of the founding CEOs of the behemoths appeared to be first-time CEOs, and the remainder had previous CEO experience at one or more companies.

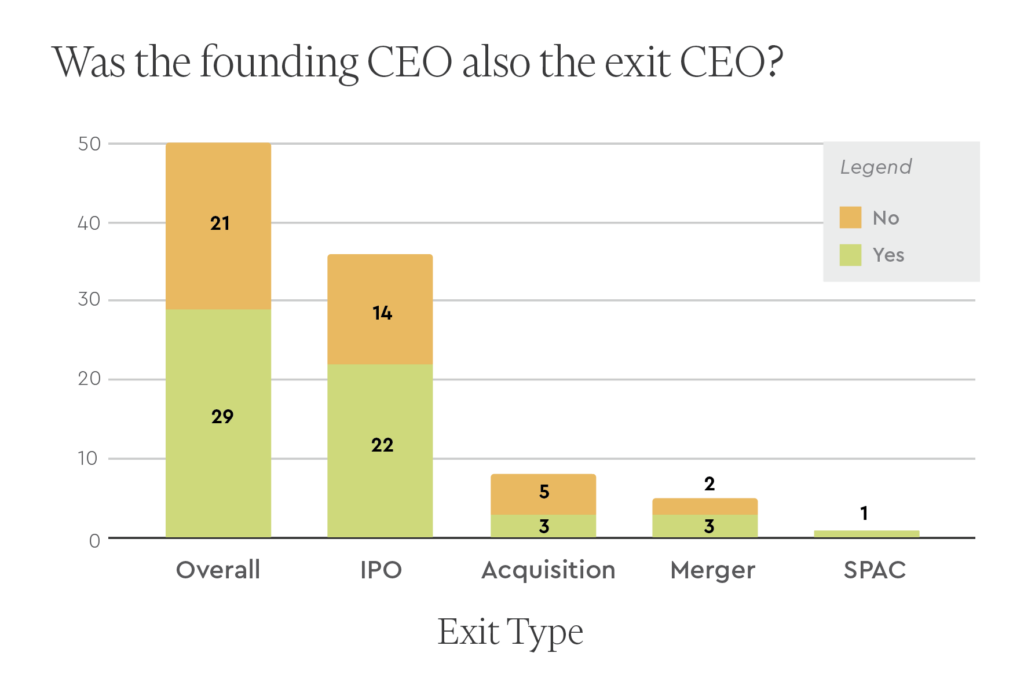

Did the Founding CEO Remain as the Exit CEO?

For 29 of the 50 behemoths, the founding CEO remained the CEO at least until the company’s initial exit (defined here as either a public financing event or an acquisition). This was more common in the case of IPOs (22 out of 36), mergers (3 out of 5), SPACs (1 out of 1), and less so for acquisitions (3 out of 8).

VC Incubation

One unique aspect of biotech venture capital is the strong tradition of hands-on company formation and incubation. To the extent we could determine based on publicly available information, the majority of the behemoths were not VC incubated, but a sizable minority (44%) were created and built by VC firms.

Among the 21 companies that were VC incubated, the firms represented most commonly were Third Rock (5 companies), ARCH (4), Atlas (3), Flagship (3), and Versant (3).

Founding CEO Equity Ownership

For those behemoths that went public, and that retained the founding CEO at IPO, we examined the founding CEO equity ownership just before the IPO. As shown below, the median CEO stake for these behemoths overall was 5.6%. Perhaps as expected, the median CEO ownership for those companies that were VC incubated (4.2%) was lower than those that were founder-led (7.4%).

Founding CEO Equity Just Before IPO

Biotech Behemoths (n=29)

VC-Led Behemoths (n=13)

Traditional Founder-Led Behemoths (n=16)

Median

5.6%

4.2%

7.4%

Mean

10.0%

6.1%

13.1%

Standard Deviation

11.5%

5.9%

14.0%

Max

54.6%

22.5%

54.6%

Min

1.0%

1.0%

2.4%

Educational Backgrounds of Founding CEOs

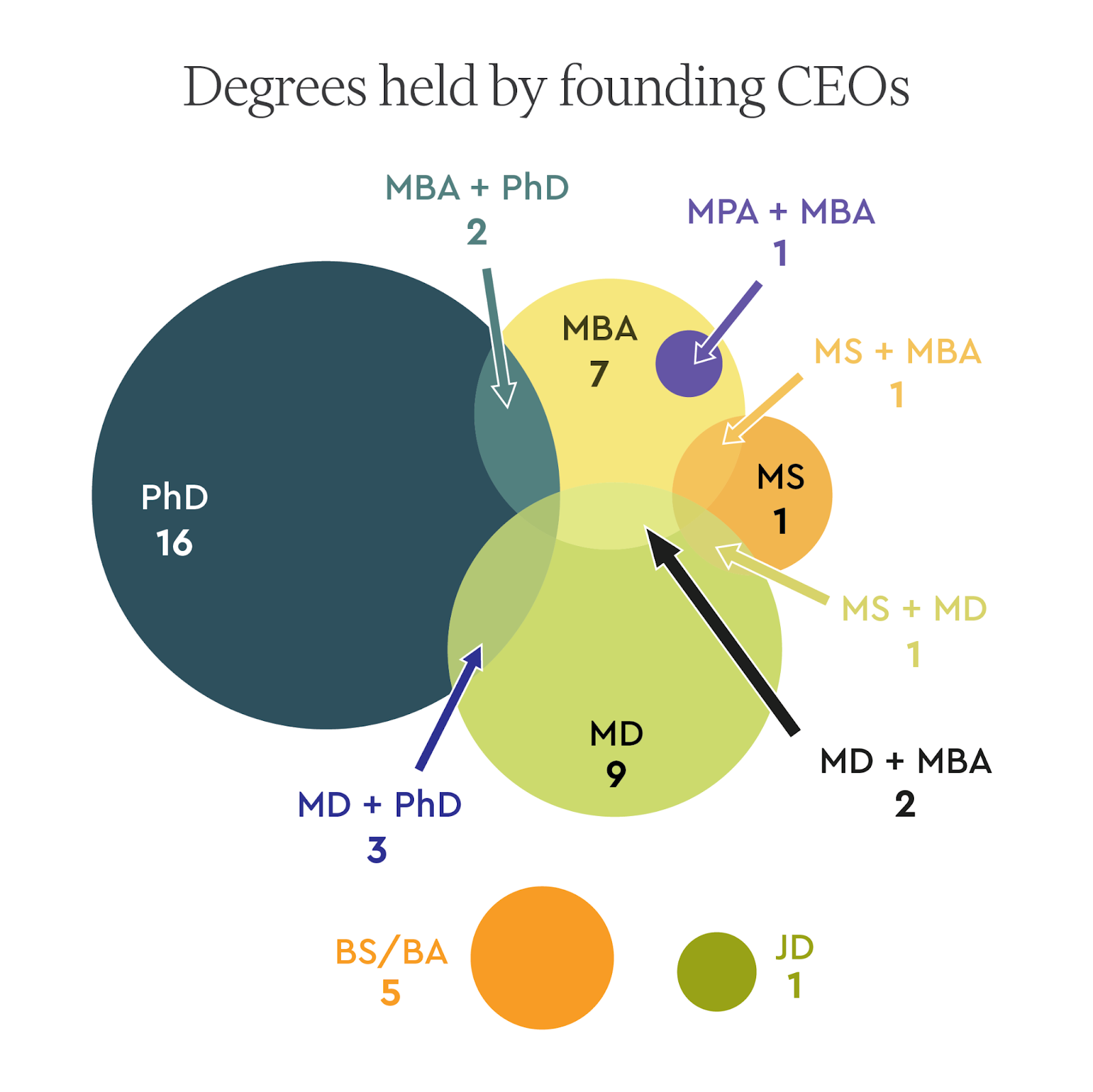

We reviewed the educational backgrounds of the founding CEOs. Of the 49 founding CEOs for whom we were able to find detailed educational data, the PhD was by far the most commonly held degree (21). The next most commonly held degree was an MD (15), followed by an MBA (13). The majority of founders held only one of these degrees, but there were a handful of MD/PhDs (3), MD/MBAs (2), and PhD/MBAs (2). Nearly all founding CEOs held a graduate degree (43), and most had specialized technical or scientific training via graduate school prior to starting their biotech company (35).

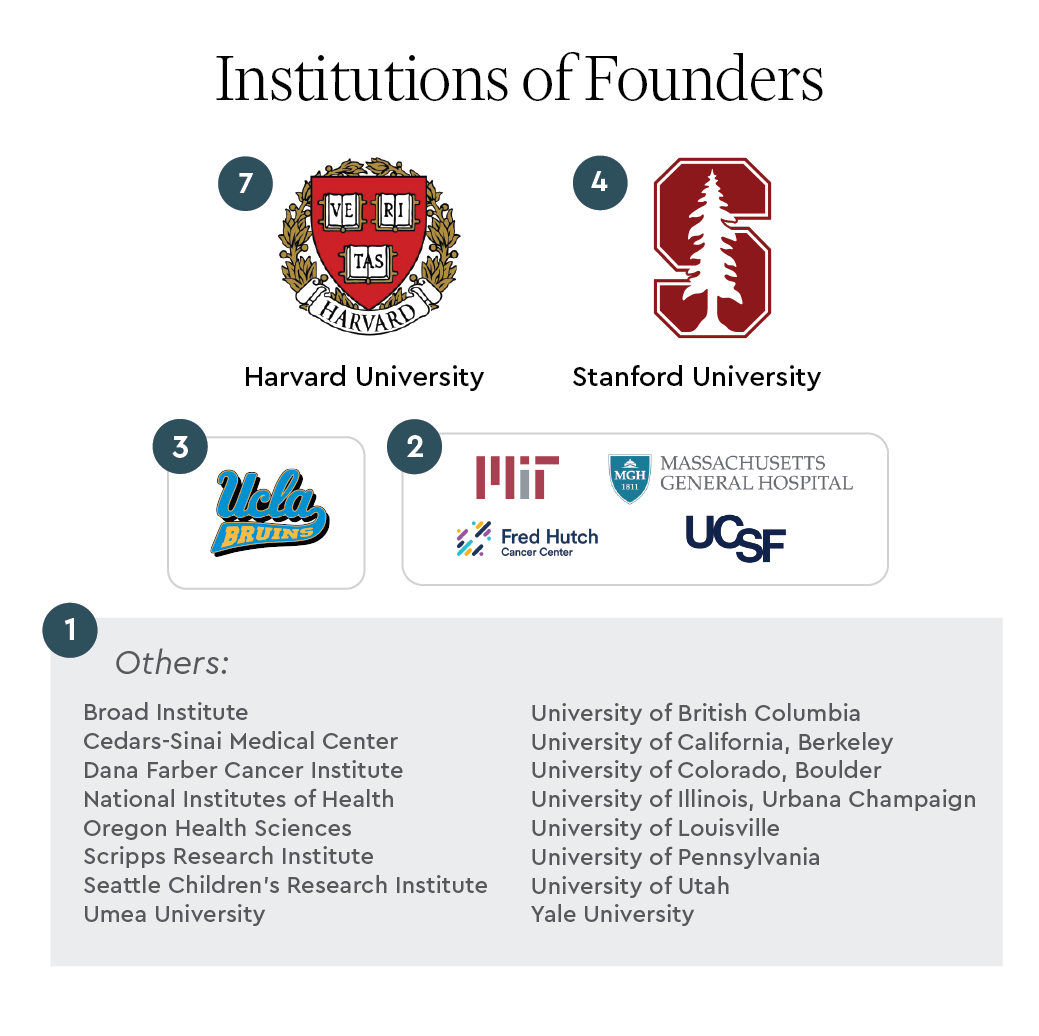

Academic Affiliations of Scientific Founders

Many biotech companies have academic roots. From our list of 50 companies, 30 had founders affiliated with at least one academic institution. The institutions that boasted the most founders were Harvard (7), Stanford (4), and UCLA (3). After these were Mass General Hospital (2), Fred Hutchinson Cancer Center (2), UCSF (2), and MIT (2).

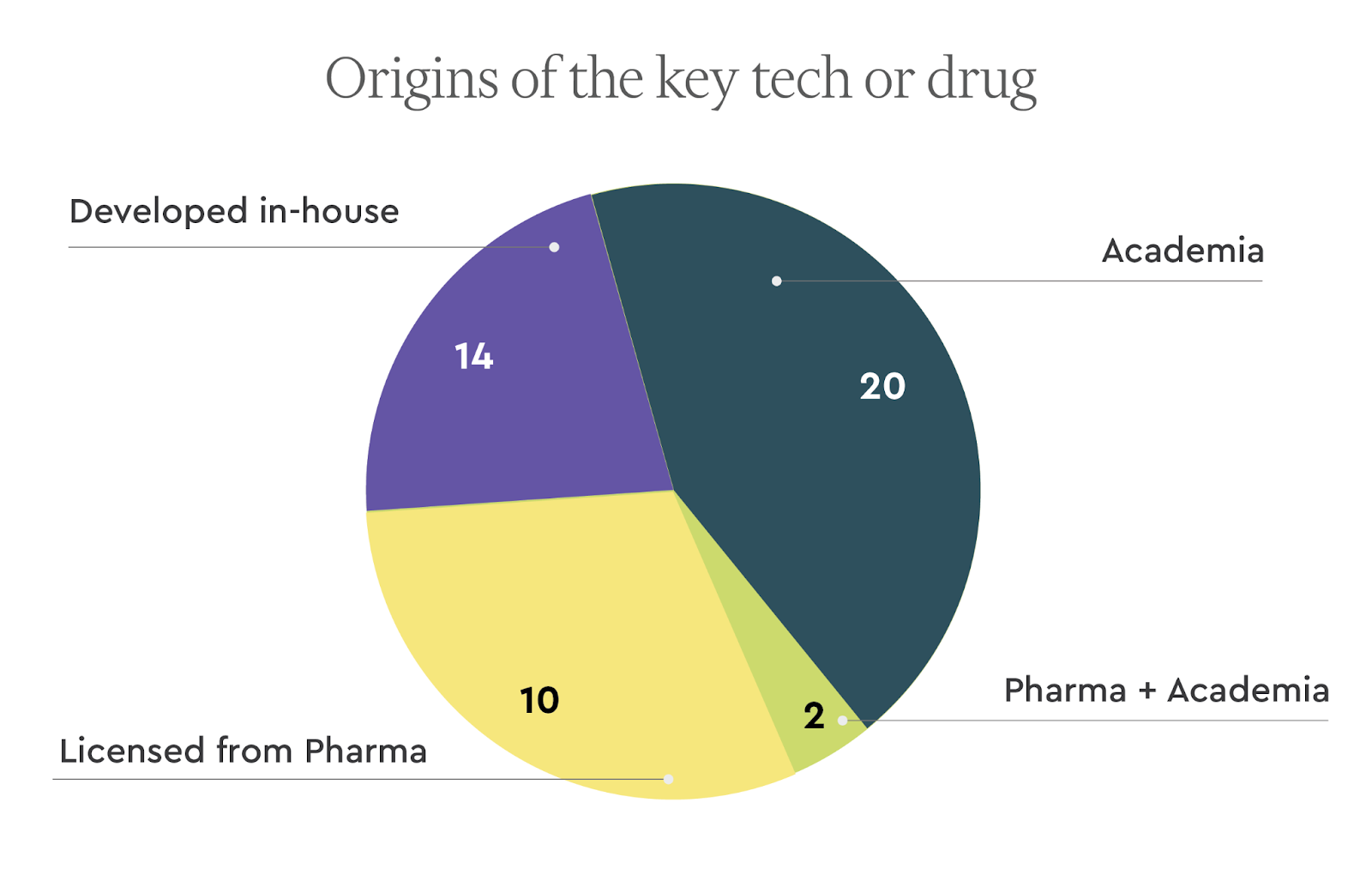

Institutions giving rise to the key technologies/drugs

Among the top therapeutics companies, the lion’s share of leading drugs originated from academic institutions. We find it interesting that 12 of these startups licensed drugs from pharma.

The research institutions that licensed out the key drugs or technologies are widely spread. The top two originating academic institutions were Stanford (4 companies) and the University of California, San Francisco (3 companies). (We combined BridgeBio and Eidos Tx here)

Global Blood Therapeutics, Sana, Revolution Medicines

Fred Hutchinson Cancer Center

2

Juno, Lyell

University of Pennsylvania

2

Moderna, Apellis

Cedars-Sinai

1

Prometheus

Children’s Hospital of Philadelphia

1

Spark Therapeutics

City of Hope

1

Juno

Genethon

1

Audentes

Harvard

1

Sana

Massachusetts Institute of Technology

1

Translate Bio

Memorial Sloan Kettering Cancer Center

1

Juno

National Cancer Institute

1

Kite

Nationwide Children’s Hospital

1

Avexis

St. Jude Children’s Hospital

1

Juno

The Chinese University of Hong Kong

1

Grail

The Scripps Research Institute

1

Receptos

UC Berkeley

1

Intellia

UC San Diego

1

VelosBio

University of British Columbia

1

Abcellera

University of Chicago

1

Provention Bio

University of Florida

1

Audentes

University of Utah

1

Recursion

University of Washington

1

Sana

Geography

Half of these behemoths were founded either in the Bay Area (15 of 50) or the Greater Boston Area (10 of 50). A significant portion was also founded in Southern California (7 of 50 in San Diego and Los Angeles).

Only three of the 50 companies were founded outside of the US: AbCellera (Canada), CRISPR Therapeutics (Switzerland), and Acerta Pharma (Netherlands), although the latter two grew to establish significant presence in Boston and the Bay Area, respectively.

Company financial characteristics:

Valuations

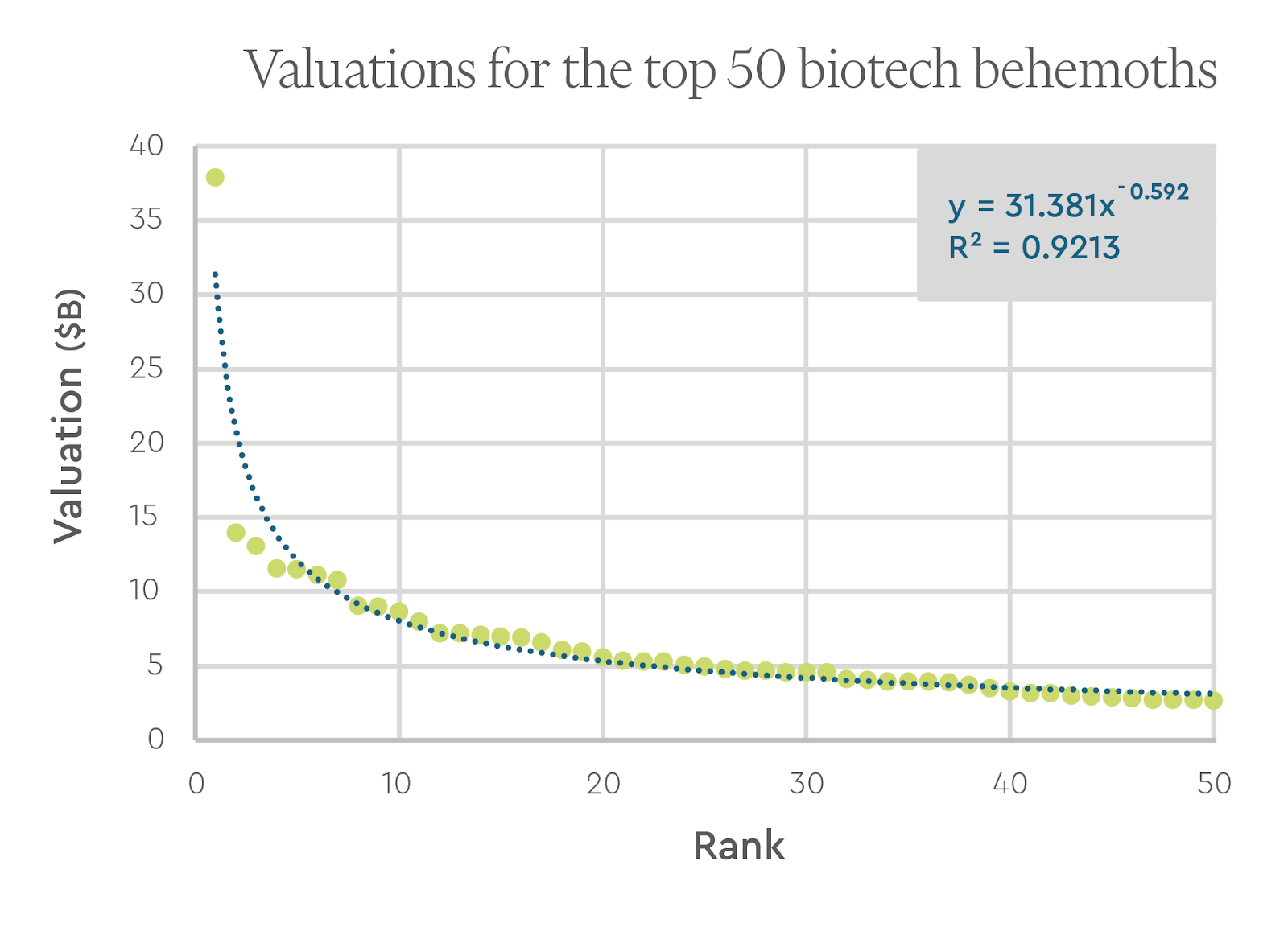

A valuation of ~$2.7B was required to make it into the top 50 companies, which represented the top 0.17% of all therapeutics and diagnostics/tools companies (~28,000) founded during the 15 year time frame. These top 50 companies also represented roughly 2.5% of all therapeutics and diagnostics/tools companies that had raised more than $50M.

These biotech behemoths are no doubt outliers. In the business of venture capital, such outliers overwhelmingly drive fund returns, and the distribution of company returns have been described by a power law. As seen below, a power law equation provides a fairly good fit for the valuations of the behemoth, although the companies in the long tail need to be included for a better estimation of the full trend.

Aggregate Multiple on Invested Capital (MOIC)

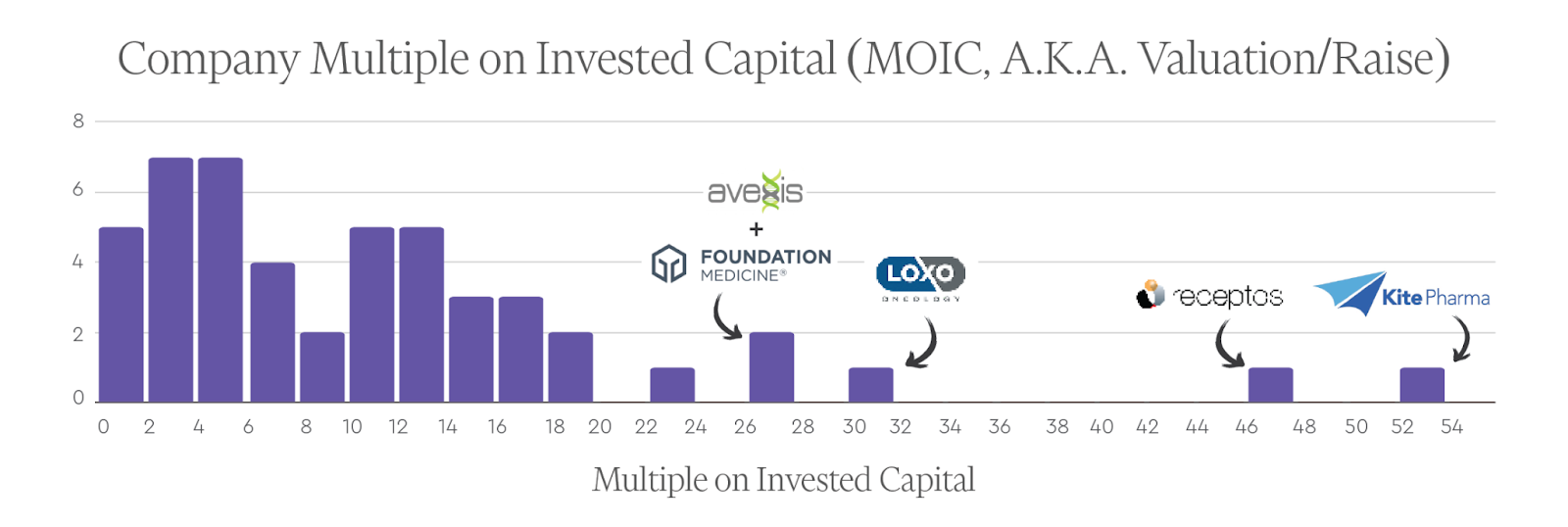

The top 50 biotech startups achieved an aggregate value of ~$322B with a total of ~$43B raised (unadjusted dollars), for a rough MOIC (here simply defined as total valuation/total investment) of ~7.5.

Individual Company MOICs

The average individual company MOIC (also defined as valuation/investment for each company) for the top 50 companies was ~11.7 and the median was ~9.7. The companies with the highest MOICs were Kite (~52.5x), Receptos (~46.2x), Loxo (~30.8x), Avexis (~27.6x), and Foundation Medicine (~26.8x).

Founding Year and Exit Year

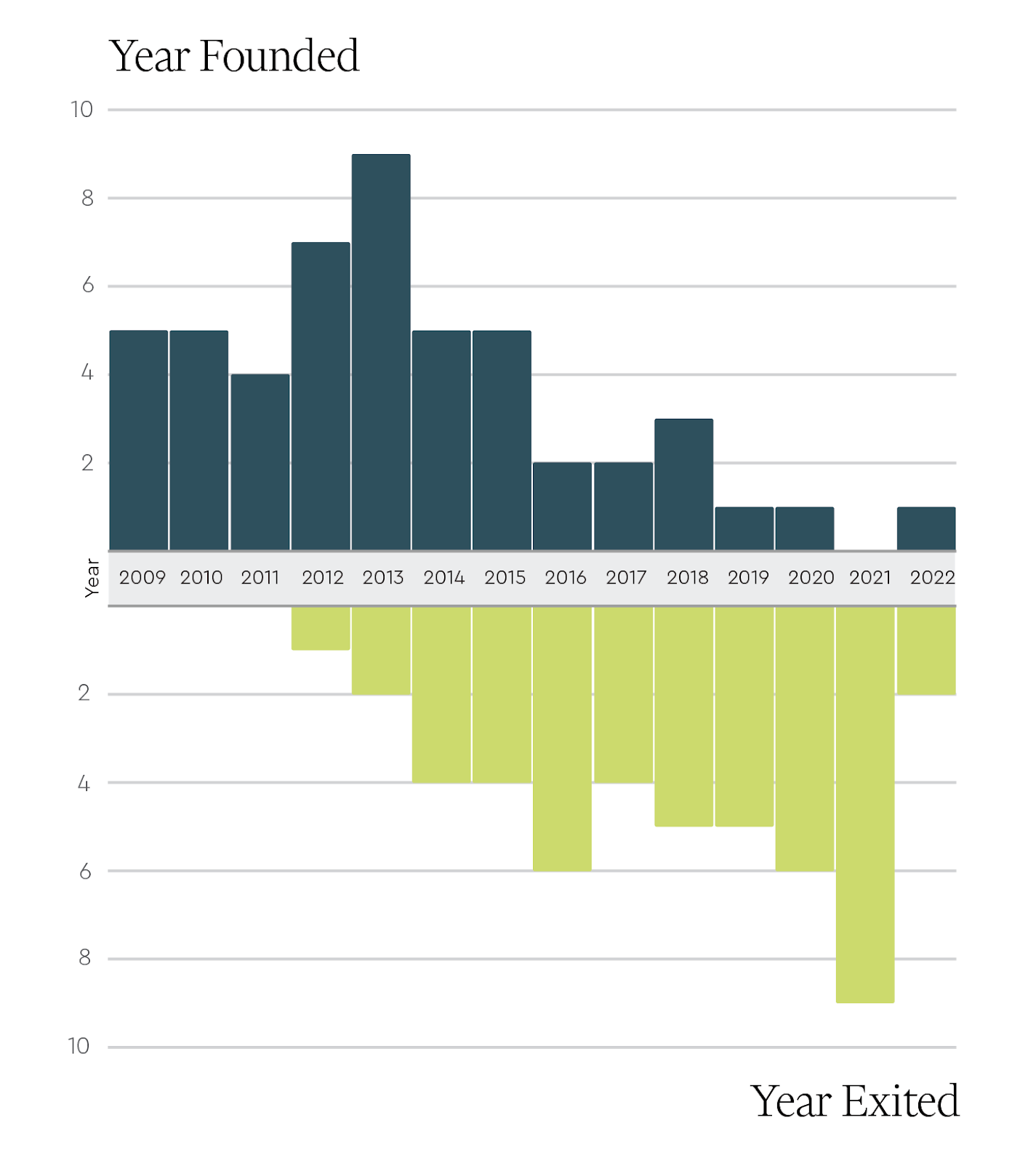

Given the time it takes for biotech companies to accrue value, the histogram of number of companies by founding year is not surprisingly skewed toward earlier years within the 2009-2023 period. Among these behemoths, the most common founding year was 2013 with 9 companies (Biohaven, Juno, Loxo, Vaxcyte, CRISPR, Spark, Turning Point, Eidos, and Recursion).

Also not unexpectedly, the year of initial exit (again, defined as either a public financing event or an acquisition) for these top 50 companies skewed later in the 15 year period and clustered around years representing favorable capital markets for biotech. 2021 was the most common initial exit year, followed by 2020 and 2016.

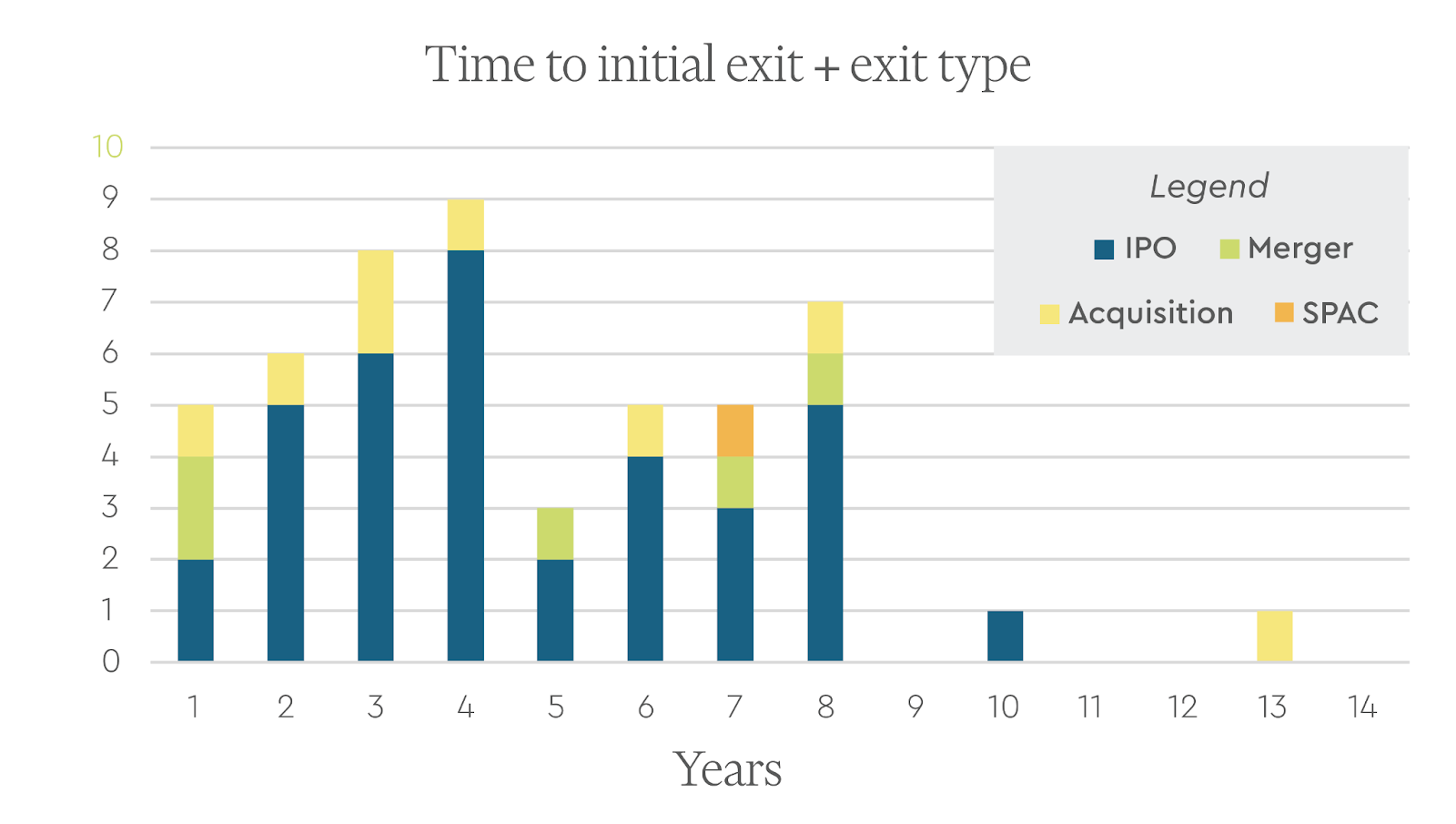

Time to Initial Exit

We looked at the number of years it took for these companies to get to an initial exit. Among these behemoths, the mean number of years was 4.7 years with a standard deviation of 2.7 years. Remarkably, 5 companies achieved an initial exit the next year after founding (Juno, Telavant, Loxo, Immunovant, and Chinook).

Comparison to top tech startups:

To contextualize selected data regarding these top biotech startups, we ran an analogous search for the top 50 tech companies founded during the same period.

The top 50 tech companies (“the tech titans”) had a higher average valuation than the biotech behemoths. Notably, the most valuable tech company on the list was Uber ($156B), worth almost 4x the most valuable biotech company, Moderna ($38B), and also worth almost half of the behemoths combined. The lowest valuation among the tech titans was $3.2B (representing the top 0.2% of all tech companies founded in the period), whereas it was $2.7B for the biotech behemoths (also representing slightly under 0.2% of biotech companies founded in the period).

For the tech titans, the average company MOIC was 23.2 and the median was 9.4. The average was driven up by companies like WhatsApp (~317x), the TradeDesk (~197x), and Honey (~56x). The average company MOIC for the biotech behemoths was lower at 11.7, though the median company MOIC was comparable at 9.7.

In aggregate, despite the many differences across these two industries, the rough MOICs of the top startups as a class looked surprisingly similar (~7.4 for tech & ~7.5 for biotech).

One key difference, however, was that the average time to an initial exit for the titans (8.2 +/-2.1 years) was considerably longer than that for the behemoths ( ~4.7 +/- 2.7 years).

Additionally, M&A was a much more important type of exit for the behemoths vs. the titans. For the biotech startups, acquisitions represented 24% of initial exits, and ultimately 52% were acquired. Only 18% of the tech companies went on to an ultimate acquisition.

We next compared the ages of the founding CEOs. The average age of the CEOs at founding for the titans was significantly younger at ~36 +/- ~8 years vs. that of the behemoths at ~46 +/- ~10 years.

Lastly, for those companies that went public, and that retained the founding CEO at IPO, we compared the CEO stake just before IPO. As seen in the summary below, the founding CEOs of the titans tended to retain more equity in their companies compared with those of the behemoths, with the median ownership in tech (11.7%) approximately double that in biotech (5.6%).

Founding CEO Equity Just Before IPO

Biotech Behemoths(n=29)

Tech Titans(n=30)

Median

5.6%

11.7%

Mean

10.0%

12.8%

Standard Deviation

11.5%

8.6%

Max

54.6%

41.5%

Min

1.0%

2.6%

Discussion and takeaways:

In this review of the top 50 biotech startups across therapeutics, diagnostics, and life sciences tools, the biotech behemoths were overwhelmingly drug companies. Even though diagnostics and tools companies undoubtedly create enormous value for patients and for the industry at large, the realities of their business models (generally lower pricing power and lower margins) render them arguably worse at capturing and retaining this value compared with therapeutics companies.

How did these particular biotech behemoths accrue such value? It’s clear that there was no one pathway to success.

Many companies focused on specialty drugs in oncology or rare disease, but two of the biggest behemoths focused on COVID and migraine, respectively – rather common indications.

Some companies developed their own products and technologies in-house, but most licensed them from academia or from other pharma companies. Some companies were VC-incubated, while many others were founder-led. Some companies brought flashy platforms to bear, but many others were asset-focused.

Some companies had experienced CEOs, but many others had first-time CEOs. Some companies boasted scientific founders from Stanford or Harvard, but the vast majority did not.

While there was an abundance of behemoths located in the key biotech hubs where capital, innovation, and management talent converge, i.e. the Bay Area and Boston, there was still a rather wide geographical spread – at least in the US. There were remarkably only 3 behemoths founded outside of the US.

Regarding the comparison between the biotech behemoths and the tech titans, most would agree that the two types of companies look radically different with respect to capital intensity, technical risk, degree of regulation, preponderance of binary outcomes, the market sizes addressed, and so on. Indeed, the most stunning successes for the behemoths paled in comparison with some of the titans in terms of both valuations and the multiples on invested capital achieved.

Yet when it came to the metric of total value created to total investment for the entire class, the overall showing for the behemoths was surprisingly similar to that of the titans.

The behemoths also tended to return capital faster than the titans due to the greater role that M&A has in biopharma (thanks to drugs continually losing exclusivity) and due to the availability of robust public capital markets to help fund expensive and risky late-stage clinical development. These findings should give prospective founders of biotech behemoths some relief.

Ultimately, what draws many to our industry is the prospect of bringing forth a new medicine that completely changes the existing standard of care; a diagnostic that adds years to a patient’s life because the disease was caught early or the right therapy was selected; or a technology that uncovers unknown biology and paves a path toward a better treatment.

By this measure, the biotech behemoths highlighted here were certainly the standard bearers for the past 15 years, developing, among other achievements, the first mRNA vaccine brought to market at a breakneck pace to address a global pandemic; a treatment for schizophrenia that precisely targets a novel pathway in the brain, while carefully avoiding side effects elsewhere in the body; the first gene therapy to restore vision to patients with an inherited blindness disorder; the first cell therapies to potentially cure a portion of patients suffering from an intractable blood cancer; genetic tests to better guide care for cancer patients; and technologies to measure the variations in the genome and the transcriptome at the level of individual cells.

What will the next generation of behemoths look like? We have a handful of predictions.

Therapeutics companies will continue to dominate. While there are headwinds with the IRA and other pricing pressures, at a high level the business model still looks favorable relative to that of diagnostics or life sciences tools, and the science is continuously progressing. We hope that we have in fact, as some data suggest, turned a corner on Eroom’s law.

Given pharma’s appetite to build on the breakthrough successes of drugs such as GLP-1 agonists for diabetes/obesity and anti-amyloid antibodies for Alzheimer’s, we can easily see several $5-15B companies being built that focus on first-in-class or best-in-class assets within metabolic disease, neurology, and immunology.

As has been the case since the birth of the biotech industry with recombinant DNA technology and companies like Genentech and Amgen, we will continue to see well-funded therapeutics behemoths founded on innovative platforms: new target discovery platforms, new methods for drug design, and new and improved modalities. For example, with the right business model and execution, a company that can truly solve extrahepatic, tissue-specific IV delivery of large nucleic acid cargoes could be worth billions in light of the plethora of valuable therapeutic payloads just wanting for delivery and the concomitant diseases that could be addressed.

We will see a few software companies for biopharma reach $3-5B. Pharma spends over $200B globally on R&D, but very little on software, and it shows. Much of the software stack in use today by biopharma R&D teams is outdated, clumsy, or fragmented. This current state, paired with the expectation that AI will impact many parts of the drug development value chain beyond target or drug discovery, suggests that eventually pharma companies will have to spend significantly more on software or risk losing their edge.

The Bay Area and Boston will continue to dominate the rankings as network effects in these hubs compound over time.

The founding CEOs of behemoths will continue to trend older than those of the titans. We think this difference in part reflects the substantial education and experience that can be crucial for founders to succeed in the complex, regulated industry of biotechnology. Perhaps as importantly, access to the substantial amounts of capital needed to achieve important value inflection points in therapeutics companies will likely continue to be gate-kept by blue chip investors who are reluctant to take on significant team risk, in addition to the many other types of risk present in these businesses.

However, we expect the founding CEO list to grow more diverse across both race and gender thanks to industry-wide efforts to promote diversity and inclusion among company boards and senior leadership teams.

We here at Pear are excited to back the next generation of such behemoths, and we can’t wait to see the impact they make on patients and our industry.

Acknowledgements:

We thank Mar Hershenson, Sarah Jones, Daniel Simon, Elliot Hershberg, and Curt Herberts for their helpful feedback and comments on earlier drafts of this review, as well as Joanna Shan for optimizing the graphics.

As a member of the Talent team at Pear, one of my primary responsibilities is assisting early-stage founders with their first hires. Each month, we receive dozens of inquiries from founders about how to best structure equity compensation for their first hires. Although there is a wealth of information available on this topic, we have yet to find a resource that effectively answers the crucial question:

How much equity should I grant my first employees?

In this post, we aim to demystify the decision-making process around equity grants for early employees and provide a practical, transparent approach for founders to use.

Summary

Benchmarking data, the most common approach founders use to determine equity compensation, is inherently flawed. It often relies on a small data set, leading to comparisons with only a few data points. It also fails to capture context, reducing the decision to a handful of variables like role, level, funding, valuation, and team size, resulting in a one-size-fits-all approach. While benchmarking data can be a helpful tool to understand the competitiveness of an offer and provide another data point to aid your decision-making, we find it is often inaccurate, especially for early-stage equity data.

To make it easier for founders, we’ve developed our own approach to equity management for early employees that captures many of the nuances missed by other methods. We refer to this process as “building an equity budget.”

Core Inputs

To start building your equity budget, you’ll need to answer the following questions:

Equity Set Aside: How much equity have you set aside for employees in your most recent raise?

Hiring Plan: How many people do you plan to hire between now and your next raise? This can be a rough estimate, but the more accurate you are here, the more precise the budget.

Position Breakdown: What specific positions are you hiring for, broken down by role type (technical or non-technical) and seniority level (senior, mid, or junior)?*

*The simplicity in role definition and leveling is intentional. We believe that a narrow and flat organizational structure is best suited for companies at an early stage.

Important Definitions & Concepts

Options Pool or Employee Equity Set Aside

It’s common for early-stage companies to set aside about 10% of shares for their employees during the fundraising process. Your employee options pool (ESOP) represents the maximum percentage of new ownership, or the number of shares, you can issue via new hire grants or refreshers to new or existing hires without further dilution. While the exact percentage you set aside will vary based on agreements with your investors, once you decide on an amount, you should avoid exceeding it.

If you haven’t raised a priced round, we suggest setting aside a certain amount of equity that functions as an ESOP, even if it’s not technically written into your agreement.

You should view your options pool as your maximum, not target, spend. Similar to managing cash burn, your goal isn’t to spend this down to zero.

We recommend setting aside a percentage of your options pool as a buffer, typically between 25-35% of the total pool. This ensures you don’t exceed your allocated resources and provides flexibility if you need to hire more aggressively or at a higher seniority level than initially planned.

Equity Allocation Guidelines: Multipliers, Premiums, and Discounts

When it comes to determining equity grants for your early-stage employees, it’s crucial to navigate through a landscape of multipliers, premiums, and discounts. Let’s break down these guidelines:

Timing Matters: Your earliest hires deserve a larger slice of the equity pie. As you bring on subsequent team members, it’s common for their equity to decrease by 20-50% with each new addition.

Technical vs. Non-Technical: Technical hires often command larger equity packages compared to their non-technical counterparts. Typically, equity packages for non-technical hires are discounted by 50% compared to their technical peers.

Junior vs Senior. Senior hires should receive more substantial equity grants compared to junior-level hires. As a rule of thumb, if equity for a junior-level hire is 1x, a mid-level hire should be 5x, and a senior hire 10x.

While these guidelines offer valuable insights, every startup is unique. You should feel empowered to tailor how you allocate equity to suit your company’s specific needs and values, but be mindful that deviations can significantly impact your equity budget.

How it works

To establish a starting point for equity grants, we recommend using 0.75% as the “baseline grant” for your first hire. This percentage represents the equity grant for a technical, mid-level employee and serves as a reference point for your future calculations. A .75% equity grant for a mid-level technical hire is consistent with market trends, based on real offers from our founders and further validated by commonly used benchmarking data.

Using the the table below, we now have the information we need to determine what size grant each hire would receive:

Buffer

25%

Discount per Hire

20%

Role Multiplier

-Technical

100%

-Non-Technical

50%

Level Multiplier

-Senior

200%

-Mid

100%

-Junior

20%

All values can be changed to align with founder preferences. However, the numbers above are considered standard and we recommend you start with similar numbers even if you end up changing them later.

Let’s assume you plan on making 3 hires in your first 6 months after raising your Seed round.

Hire #1: Senior Technical

Hire #2: Senior Technical

Hire #3: Mid Non-Technical

Using the tables below, you can easily calculate what your equity spend would be in your first 6 months.

Equity for Hire #1: Senior Technical

Role

Level

% After Discount

Baseline Grant #1

Role Multiplier

Level Multiplier

Equity Grant

Technical

Senior

100%

.75

100%

200%

1.50%

Technical

Mid

100%

.75

100%

100%

0.75%

Technical

Junior

100%

.75

100%

20%

0.15%

Non-Technical

Senior

100%

.75

50%

200%

0.75%

Non-Technical

Mid

100%

.75

50%

100%

0.38%

Non-Technical

Junior

100%

.75

50%

20%

0.08%

Equity for Hire #2: Senior Technical

Role

Level

% Post Hire Discount

Baseline Grant #2

Role Multiplier

Level Multiplier

Equity Grant

Technical

Senior

80%

.60

100%

200%

1.20%

Technical

Mid

80%

.60

100%

100%

0.60%

Technical

Junior

80%

.60

100%

20%

0.12%

Non-Technical

Senior

80%

.60

50%

200%

0.60%

Non-Technical

Mid

80%

.60

50%

100%

0.30%

Non-Technical

Junior

80%

.60

50%

20%

0.06%

Equity for hire #3: Mid Non-Technical

Role

Level

% Post Hire Discount

Baseline Grant #3

Role Multiplier

Level Multiplier

Equity Grant

Technical

Senior

64%

.48

100%

200%

0.96%

Technical

Mid

64%

.48

100%

100%

0.48%

Technical

Junior

64%

.48

100%

20%

0.10%

Non-Technical

Senior

64%

.48

.50%

200%

0.48%

Non-Technical

Mid

64%

.48

50%

100%

0.24%

Non-Technical

Junior

64%

.48

50%

20%

0.05%

Your total equity spend would be 2.94% which leaves you with a little over 60% of your available equity pool left to spend on your remaining hires.

Hire

Role

Level

Grant

#1

Technical

Senior

1.50%

#2

Technical

Senior

1.20%

#3

Non-Technical

Mid

0.24%

Total

2.94%

Remaining

4.56%

Startup Equity Calculator for Early Hires

To help illustrate this approach even more clearly, we’ve built acalculatoryou can use to perform this exercise on your own.

Final Notes

For growing companies, the primary constraints on equity grants are the size of the options pool set aside for employees and the number of hires a company plans to make. For example, if Company A plans to hire 10 employees and Company B plans to hire 20, but both have the same size options pool, Company B will have less equity to allocate per employee.

Companies with significant hiring plans (greater than 10 hires) should establish a minimum baseline for equity grants. This approach is reflected in the “Min Baseline Equity” section of our calculator. It ensures that equity grants do not fall below a certain threshold, counteracting the rapid decrease in baseline equity from Hire 1 (0.75%) to Hire 10 (0.10%). The figures shown in the example above assume a 20% decrease in the baseline equity grant with each subsequent hire.

Upon reaching Series A, companies often move from the “Discount Per Hire %” approach to a standardized system where all employees in the same role and level receive equal equity grants. For Series A companies, we suggest resetting the baseline equity grant for a mid-level technical hire to 0.075%.

Many candidates at this stage expect grants that fall outside typical ranges. Running candidates through this exercise can provide them with the context needed to better understand the size of their grant.

Most importantly, we recommend doing whatever is necessary to close the right talent, flexing where needed to hire outlier candidates. This post about Minimum Fundable Teams captures some of our thoughts on why the right team is so important.

We hope you found this resource helpful. Visit our Talent Services page to learn more about our team and the work we do to support founders.

Last week, PearX S21 alum, Valar Labs, announced its $22 million Series A round co-led by DCVC and a16z with participation from Pear. We’re incredibly excited for this milestone for Valar Labs and wanted to take this opportunity to look back on our history working with their team.

We met the Valar Labs co-founders at a free boba event we hosted on Stanford’s campus in 2020. After that first meeting and introduction, the Valar Labs team applied to Pear Competition. And from there, they joined our PearX S21 cohort.

PearX S21 cohort, which included companies including: Valar Labs, Kale, and Aklivity

When we met the team, we were incredibly excited to back them for a few big reasons:

This is a massive and unsolved market opportunity. Valar is using AI to help oncologists choose the correct treatment for their patients. Unfortunately, for thousands of cancer patients each year, there is a high degree of uncertainty around which treatment option works best for them. This uncertainty leads to billions of dollars of potentially unnecessary drug costs, and even more importantly, wastes precious time for thousands of patients battling cancer. The sad reality is that most cancer patients end up on a treatment sequence that fails them, and Valar Labs is on a mission to change that.

The team had a clear vision for the type of product that could best meet this unmet need. Valar is truly a software company that enables capabilities that legacy diagnostic companies do not have. Unlike many diagnostics companies for which the core technology revolves around a novel laboratory assay, Valar uses AI to analyze images of a patient’s tumor and to predict the likelihood of response to different standard-of-care treatments. This information helps oncologists determine the best treatment pathway for a patient.

The team was well suited to tackle this problem: Valar’s co-founders, Anirudh Joshi, Viswesh Krishna, and Damir Vrabac, met at Stanford in 2020 when they were all part of Dr. Andrew Ng’s machine learning group. While at Stanford, they had the opportunity to spend time at the intersection of AI and medicine, speak to hundreds of oncologists, and find the key areas of high medical unmet need. Not only were they had were innately curious and incredibly quick learners, they also gathered the most esteemed KOLs in the space including Professor Eric Collison from UCSF and Professor Pranav Rajpurkar from Harvard/Stanford to solve this problem.

The team hit the ground running during PearX, and the Pear team was there to assist them in hiring their first employee, introduce them to strategic advisors on both go-to-market and the clinical side, and get their story in shape for fundraising. While whiteboarding with the team, it was clear that to be successful, they needed data access and partnerships with cancer centers.

Valar’s Demo Day pitch in October 2021

Upon completing PearX, Valar hit a number of milestones in their company growth. After Demo Day, Valar Labs closed their seed round of $4.15M led by the a16z Bio + Health fund. They’ve leveraged their seed funding to reach clinical validation and form partnerships with top academic and medical institutions, and they’ve unveiled Vesta, the first-ever, AI-based oncology test for bladder cancer.

Anirudh and the Pear team

When we first met Valar Labs, they were 3 founders operating out of a dorm room. Now they are more than 14 employees with $26M raised. Their growth path has been incredible to date and we know the best is yet to come for this team.