Every founder needs to become an expert at fundraising to build a successful venture scale company. It’s not just about the tactics, but having the right foundation for your company and a compelling pitch that answers key questions about your market and generates excitement.

Orby AI recently announced its $30 million Series A round, co-led by NEA, Wing Venture Capital, and WndrCo, with participation from Pear VC. We are proud to be Orby’s earliest investors (when a LinkedIn message from their CEO first connected us) and we are thrilled to continue our support now.

Orby’s Enterprise AI Automation tool automates complex workflows by observing users at work, identifying repetitive tasks, and writing the code to automate those tasks. Within minutes, a custom automation is ready to be implemented with user approval.

This is game changing.

Orby AI is Changing the Game by Disrupting Process Automation Market

Co-founder and CEO Bella Liu was heading AI Product at UI Path, a leading business automation software company, when she was first inspired with the idea behind Orby. At the time, the RPA (robotics process automation) software being used relied on human users to input specific “if this, then that” rules, which turned out to be rather fragile. For example, a user who frequently opens invoices and transfers numbers to a spreadsheet must specify exactly which buttons to click and where on the screen those buttons will be— a system that is prone to error, slow, and hard to scale.

Orby AI’s Model Learns and Implements Without User Input

Orby’s approach to business automation is a huge leap forward. Unlike traditional RPA models, Orby’s LAM (Large Action Model) approach means their product doesn’t need to be told which tasks to automate, or how. Orby simply observes a user at work, learns what could be automated, and creates the actions to implement it. The user just approves the process and can correct the model at any time, thus continuously helping Orby improve.

Why We Chose Orby AI

We’re very excited about Orby’s team. Co-founders Bella Liu and Will Lu bring deep experience and expertise in the AI and automation technology space. Bella (CEO) was previously the AI product leader at UiPath, from early-stage to post-IPO. Will (CTO) was previously the data platform leader at Google Cloud AI and was involved in three AI products with real world deployments within Google. Orby’s team was a great founder-market match for Pear’s thesis on AI automation for human to machine and machine to machine automation. We are pleased to have backed Orby early on, and remain certain they are the right group to work on this problem.

What Orby AI Does

Before partnering with Orby, the Pear team was already deeply interested in AI automation for enterprise applications, aiming to solve specific problems within distinct industries one vertical at a time. They believed that the kinds of AI tools which could understand specific use cases, gather necessary datasets, and execute targeted solutions were the future. Additionally, they had a thesis that semantic understanding of workflows, enabled by backend interaction data, could enhance the generalizability of RPA.

Orby’s team embraced a similar approach but expanded it to build a horizontal enterprise AI automation platform applicable across many verticals. Initially focusing on widely used workflows like invoice processing and expense auditing, they aimed to enhance their action-based foundational models. This led to the creation of a platform that delivers immediate value in various enterprise scenarios while achieving general-purpose AI automation.

Orby is pioneering a Generative Process Automation (GPA) platform, leveraging the industry’s first Large Action Model (LAM) for enterprise use. This platform enhances efficiency by enabling teams to automate complex tasks independently. Orby’s multimodal large action model, combined with an AI agent capable of symbolic reasoning and neural network analysis, seamlessly handles intricate automation requests.

When tasked with an assignment, Orby’s AI autonomously generates workflows, integrating with specialized AI agents for sub-tasks such as data analysis or customer interaction. By learning and automating workflows contextually and semantically, Orby surpasses traditional RPA systems. The LAMs empower Orby’s AI to understand and automate repetitive processes across unstructured datasets, emulating human capabilities.

This neuro-symbolic programming captures standard process flows and ensures robust exception handling, making AI-driven automation accessible and efficient for enterprises. Orby’s patented technology, which combines LAMs with advanced programming techniques, empowers workers to automate tasks without needing technical assistance. The system continuously learns and adapts, improving productivity and efficiency over time.

Market Opportunity

The market potential for automation in enterprises has been evidenced by the success of Robotic Process Automation (RPA). However, AI Process Automation, like that offered by Orby, goes beyond traditional RPA by making previously uneconomical use cases viable. The return on investment (ROI) for RPA is often hindered by high implementation and maintenance costs, limiting its applicability.

Orby’s innovative approach addresses two critical challenges of RPA:

1. Semantic understanding of automatable workflows versus fragile rule-based systems.

2. Hands-off, continuous online learning and improvement of both workflow discovery and implementation.

By discovering automatable repetitive workflows and generating maintenance-free AI automations, Orby significantly reduces implementation and maintenance costs. This makes a much larger share of repeatable workflows candidates for automation, substantially improving ROI and expanding an already large market.

This advancement is not merely an efficiency gain for high-volume, repeatable workflows. Imagine an AI capable of automating any workflow, regardless of volume, simply by demonstrating the process. This capability would enable enterprises to innovate their workflows at an accelerated pace, shifting focus to strategic improvements. In this competitive landscape, no enterprise can afford to ignore such technology, as those who adopt it will innovate faster.

To provide a baseline, a 2017 McKinsey Future of Work report estimates that 60% of jobs involve at least 30% repetitive tasks that can be automated. Orby has already demonstrated massive productivity gains in several Fortune 500 companies through successful use cases. This is just the beginning; the market opportunity is far greater.

How we partnered together

After funding Orby’s seed round in July 2022, in addition to our close partnership on product and vision, we leveraged the full Pear team to partner with them in the following two years. Ana Leyva and Pepe Agell worked with the Orby team on their product-market fit and GTM strategy, and Jill Puente helped them in marketing and PR, including landing the Business Insider piece announcing the initial seed round. Nate Hirsch from Pear’s talent team helped Orby hire eight out of their first ten team members (eight engineers, two designers, and a recruiter). When it was time for Orby’s Series A raise, the company went through Pear’s fundraising bootcamp with Mar’s full support behind them. As we say to founders at Pear: if you get one of us, you get all of us as partners.

We’re excited to have been supporting Orby AI since day one and look forward to their promising journey ahead!

Last month, PearX S21 alum Transcera announced its seed round led by Xora Innovation, joined by Tau Ventures and existing pre-seed investors Pear, Digitalis Ventures, and KdT Ventures. To mark this milestone, we wanted to share more about Pear’s partnership with Transcera and its founders, Hunter Goble (CEO), Justin Wolfe (CSO), and Wayne Lencer (scientific co-founder).

We first met Hunter and Wayne when they applied to Pear Competition. Hunter was still an MBA student at HBS and Wayne was a professor at Harvard Medical School and researcher at Boston Children’s Hospital. At the time, they were part of the Nucleate program and looking to commercialize a new drug delivery platform they were working on.

S21 PearX Demo Day

When we met the team, we were excited about Transcera for several reasons:

Enormous unmet need and market opportunity. Today, many of the most impactful and best-selling medicines are so-called biologic drugs, comprising complex molecules that are typically synthesized via living systems rather than chemical means. These are large, bulky molecules including peptides or proteins that often exhibit little-to-no uptake upon oral dosing, and instead have to be injected into the blood or under the skin. For obvious reasons, when given a choice, patients strongly prefer the convenience of a self-administered pill. For example, pharma companies are now racing to develop orally administered versions of GLP-1 receptor agonists for obesity, as the first such drugs approved for this blockbuster indication have required administration via subcutaneous injection.

Broad, differentiated, and defensible technology platform – inspired by nature, informed by high-quality science, and validated preclinically. For almost three decades, Wayne and his group have been studying how large, orally ingested bacterial toxins, such as cholera toxin, are able to cross the intestinal epithelial barrier to cause disease. The lab discovered that structural features of key membrane constituents called glycosphingolipids directly influence the cellular sorting of these lipids and any associated payloads. Building on this foundational work, Transcera has demonstrated preclinically that synthetic lipids can be harnessed to achieve transport of biologics across intestinal barrier cells, enabling oral delivery and enhanced biodistribution. This active transport mechanism is differentiated from most existing approaches to enhancing oral bioavailability, which have primarily focused on passive diffusion enabled by permeation enhancers and other formulation excipients, and have suffered from relatively low absorption and narrow applicability.

Ambitious operating team with complementary skill sets. Prior to HBS, Hunter spent 5 years at Eli Lilly working on the commercial launch of a key drug product, and he also served as an internal consultant around new product planning for the pharma company’s immunology division. Justin completed his PhD in the Pentelute lab at MIT where he focused on delivery strategies for biologic drugs, including novel conjugation approaches for peptides, and he later worked as a scientist advancing the discovery and medicinal chemistry of macrocyclic peptides at Ra Pharmaceuticals through its acquisition by UCB. Whereas Hunter brings a savvy commercial mindset and disciplined financial rigor to Transcera, Justin in turn brings apt academic and industry domain expertise and strong scientific leadership skills. Hunter, Justin, and Wayne all share a passion for translating basic science research into technologies and programs that can make a tremendous impact for patients.

We have been impressed with the Transcera team’s execution and scientific progress so far. During PearX S21, we worked closely with Hunter on shaping the story and crafting the pitch ahead of Demo Day. Before joining the Pear team full-time as Pear’s biotech partner, I served as an industry mentor to Transcera, advising the team on questions related to IP in-licensing. After joining Pear, I continued to work closely with Transcera and fellow syndicate co-investors on scientific strategy, fundraising, and partnering.

The full PearX S21 cohort after Demo Day

Over the past two years, the Transcera team has proven to be resilient and resourceful. The production and scale-up of the synthetic lipid conjugates were challenging to master, but the team’s diligent efforts yielded multiple promising lead compounds. Critically, the team has expanded to bring in hands-on expertise in chemistry, cellular biology, and preclinical development, among other areas.

With this recent financing, we are excited to continue to back the Transcera team, and we are eager to see further development of the platform, with the ultimate goal of unlocking the full potential of biologic drugs for patients.

The Transcera team is hiring! Please check out the job posting here: https://jobs.polymer.co/transcera/28175. If you’re interested please reach out to Eddie and we can connect you!

Honey Homes, closed their Series A recently, led by Khosla Ventures and supported by Pear and others. To mark the occasion, we thought we’d do a little lookback of our history working with the Honey Homes team over the last few years.

We were first introduced to Honey Homes’ Founder and CEO Vishwas Prabhakara through DoorDash alums, including Evan Moore. The Khosla team knew that the Honey Homes team had a promising early idea and felt Pear would be great seed partners in shaping it into a venture-scalable business.

Once we met the team, we were excited about backing them for a few key reasons:

First of all, we knew this was a massive and unsolved market opportunity. US homeowners spend $250 billion annually on their homes via a highly-fragmented vendor network. The Honey Homes team saw a big opportunity to streamline that network and create a product experience that has never existed for home owners. Most home services companies are marketplaces or managed marketplaces, so it is challenging to make the economics work and keep the quality bar high while scaling. This results in churn from both the supply and demand side. Honey Homes saw an opportunity to do things differently and build out a new model – a homeowner subscription business where they employ handy people. This changes the economics and raises the quality bar substantially.

Secondly, they had a clear vision for a product to meet that market demand. The Honey Homes team wanted to build a membership service for busy homeowners to manage and complete to-do lists. I was a new homeowner myself at the time, could easily relate the never ending list of tasks to maintain my home and the difficulty of finding and keeping handymen. I found the idea of a reliable membership service really enticing.

Finally, we felt that the team was really strong and perfectly suited to tackle this problem. Vishwas was Yelp’s first General Manager and he was also COO of Digit, where he gained valuable experience as an operator. He understood first hand the piecemealing that homeowners have to do for maintenance and improvement work. Avantika Prabhakara, who leads Marketing at Honey Homes, has a rich marketing background from organizations like Opendoor, Trulia, and Zillow, so she’s also deeply familiar with the challenges people face on finding reliable contractors and handyman services.

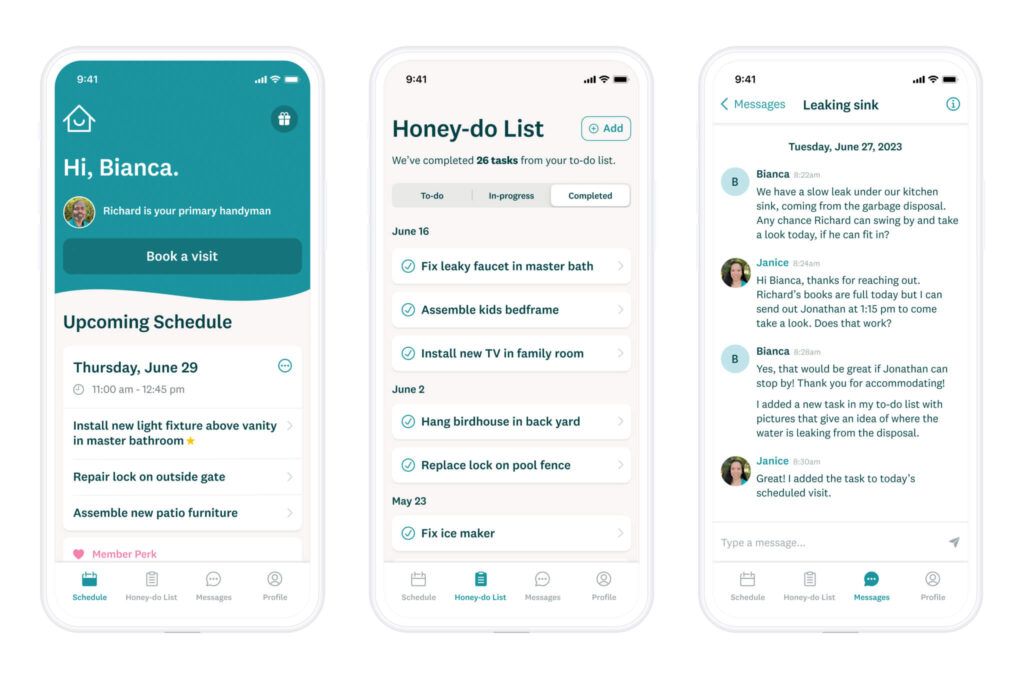

The Honey Homes app is easy-to-use for homeowners.

Khosla and Pear co-led the seed round in July 2021. Over the last two years, they’ve focused on building out the infrastructure to make this service work, growth in their initial markets, and eliminating key risks in order to raise their Series A. They grew from just a co-founding team to 12 employees and 14 handymen during this time. They also expanded across the Bay Area and Dallas and onboarded 500+ subscription customers. In total, over 20,000 home tasks have been completed for members through more than 10,000 Honey Homes visits over the last two years.

I’ve been lucky enough to not only be an investor into Honey Homes, but also an early customer. I started using Honey Homes in March 2022, and I’ve had hundreds of tasks completed in my home ranging from fixing a frustrating leaky pond to helping us move our furniture to fixing water-damaged cracks in our ceiling to cleaning out dryer ducts. We use the service so regularly that even my daughter knows our handyman, Miguel, by name. Honey Homes has had an incredibly strong customer response: everyone who hears about it wants to join and they’ve done an excellent job retaining customers.

We’re so proud of the team for successfully raising their Series A and cannot wait for their continued growth and success!

We first met Federato’s Co-founders Will Ross and William Steenbergen in March 2020, when they were first year grad students at Stanford’s Graduate School of Business. They were winners of the 2020 Pear Competition and we also invited them to join PearX, our early-stage bootcamp for founders.

The early Federato team.

When we met Will and William, they only had a product concept and some initial customer validation. But even though they didn’t have solid proof yet, we decided to partner with them in building Federato for a few key reasons:

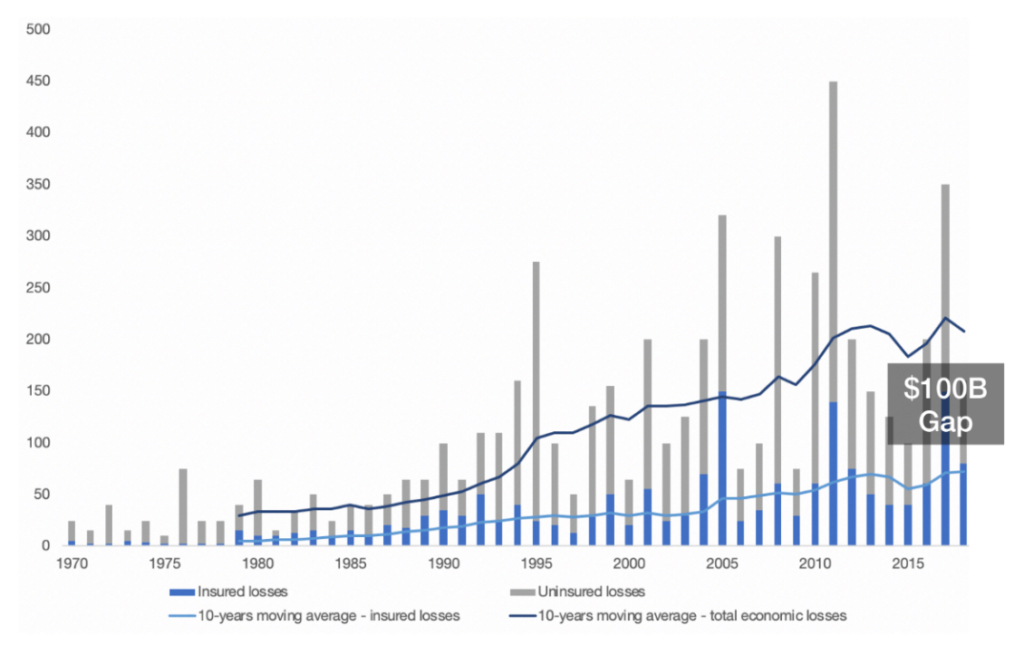

First, we saw a big market opportunity. New risks like climate change, cyber security, and social inflation were changing the landscape. In the insurance industry, risk is the opportunity, and it’s a really hard problem to solve. Insurers operating processes are unable to accommodate emerging risks, but Federato brought a solution to the table to help insurers take on risks of under utilized data assets. We knew at the time that climate change was already affecting the insurance industry in dramatic ways. The elevated frequency of damaging weather events drove more than $100B in uninsured losses between 2018-2019 alone, and this number has only continued to grow since then.

Elevated frequency of weather events drove more than $100B in uninsured losses in 2018-2019. Read more: SwissRe “Closing the Protection Gap Together”

Second, even though they were early in their journey, the founders had a clear vision. We believed in their vision to bring AI into how insurance companies manage the risks associated with an ever-changing world, including the elevated frequency of damaging weather events caused by climate change. They concluded that the best way to achieve this was through a federated learning mechanism (hence the name Federato) that would allow insurance companies to benefit from their own data, as well as other entities’ and insurance companies’ data, safely. We also appreciated that their solution delivered a simple, convenient, and beautiful UX experience, where every interaction was optimized for the user.

Third, we believed in the team from the get go. In their early days, they described themselves as “two deeply passionate, data science/product people who came together to do something about climate change with machine learning.” Will conceived of the concept behind Federato when he was an Associate at Venrock and William built ML models for the insurance industry at his prior startup, Building Blocks. Together, they researched and deeply understood the space. They didn’t just bring us an idea on a slide deck, but instead they brought a thoroughly thought out plan with multiple in-depth customer interviews, a light proof of concept built on publicly available data, and a clear understanding of the end user and end buyer. We could see that this was a team with a clear analytical mind and a bias for action, which is a rare occurrence.

During PearX, the team coined the term RiskOps, which is about realizing that risk cannot be priced without taking distribution into account. This is a tricky concept to explain clearly, but we worked closely with them to articulate this vision at Demo Day. We also partnered closely with Will and William in developing the first version of their operational underwriting software that continuously monitors risk at every underwriting decision, rather than only a few times per year. Arash and I remember working together to create hand drawn mockups of their initial software over long Zoom meetings during the height of Covid lockdowns.

Federato’s Co-founder Will presented to thousands of investors during PearX’s first ever virtual Demo Day at the height of the COVID pandemic in 2020.

Shortly after presenting at Pear’s S20 virtual Demo Day, Federato closed a Seed round led by Caffeinated Capital. Between their Seed and Series A rounds, we worked with them on important company-building milestones, like refining the product, building a strong company culture, and navigating long sales cycles through acquiring their first few customers.

We also helped the Federato team prepare for a successful Series A raise through our Series A Bootcamp. They successfully raised their Series A from Emergence in 2022.

Federato sharing their vision and progress with Pear’s team and investors in 2022.

In less than a year following the Series A raise, Federato proved itself even more. They truly became an economically efficient marketplace that connects data to the value it can actually create in underwriting. In this year, Federato team tripled their customer base, doubled their spend with existing customers, and entered new segments.

Riding off of this strong momentum, they just closed their Series B round from Caffeinated, Emergence, and Pear, and we’re excited to continue working with Will, William, and the entire (growing!) Federato team on their mission to modernize the insurance industry!

Last week, PearX S19 alum WindBorne Systems announced their $6M seed round led by Footwork Ventures and joined by Pear, Khosla Ventures, and others. We love WindBorne’s founding story as it embodies everything we believe at Pear about mission-driven, high perseverance founders.

I was lucky to meet the founders of WindBorne back in the spring of 2019, when they were undergraduate students at Stanford University. They showed up to my office hours with a balloon in tow, similar to the one pictured below.

Early prototype of a WindBorne balloon

I had no idea that the homemade-looking device was a low cost, highly durable weather balloon that could fly at a wide range of altitudes. They called this balloon ValBal for (Vent to sink, Ballast to rise).

We decided to partner with WindBorne for two reasons:

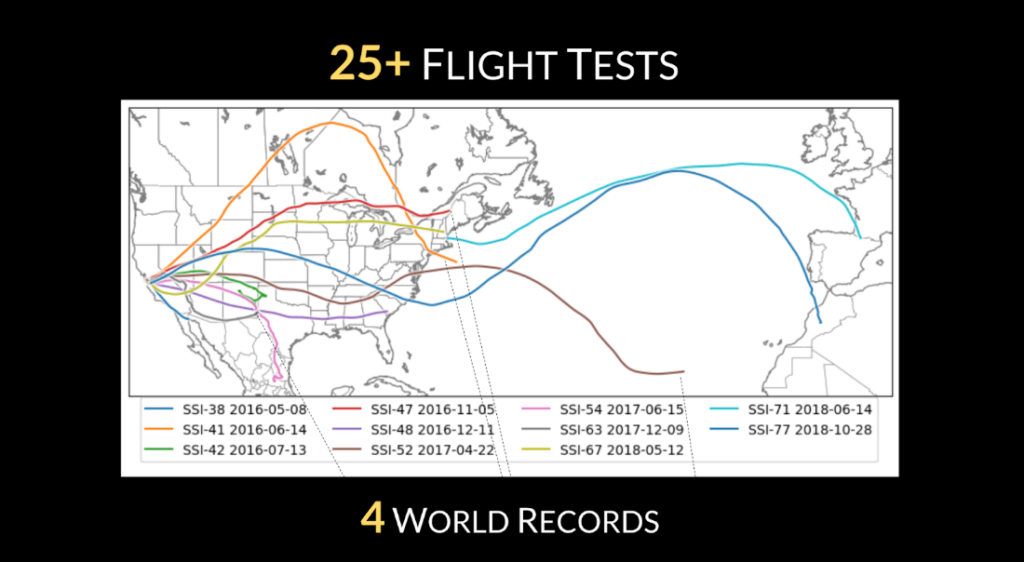

First, we believed in the founding team. They had demonstrated a clear mission, a strong passion, and an incredible ability to execute. They’d been addicted to this idea since they were freshman at Stanford as members of the Stanford Student Space Initiative. Constrained by a student budget, they used ingenuity and engineering to build weather balloons that would fly for a few hours and then pop. Over the years, they kept adding sensors and extending flight time, steadily improving their product. By the time I met them, they had already completed 26 test flights and broken four world records.

Map of flight tests the WindBorne team conducted while in college

Second, they were capturing data that no one else was capturing. At the time, we were not 100% sure of the value of such data, but after making a few calls, we discovered potential customers were interested in learning more about what the balloons could do.

WindBorne team testing balloons during their time at Stanford

With that, we invited WindBorne to join PearX’s Summer 2019 cohort, where we partnered closely with the founders to understand the most attractive market opportunity to go after. Through customer interviews, they discovered a massive data gap: only about 15% of the Earth’s surface has regular in-atmosphere observations, but weather is a global system. To better predict the weather, you need better weather data. Existing technologies couldn’t plug that gap, because the laws of physics prevent satellites from collecting the most critical weather observations. That’s where balloons come in: they’re able to collect data where satellites can’t.

Kai during PearX Summer 2019

Investors were convinced of the potential, and following S19 Demo Day, Windborne closed a successful seed round led by Khosla and Ubiquity Ventures. They spent the last four years growing the company: from iterating on their go-to-market strategy to team building to customer interviews to strategy sessions and more. We had the privilege to work side-by-side with John, Kai, Joan, Andre, and the entire WindBorne team every step of the way.

WindBorne team at PearX 2019 Demo Day

Last fall, the WindBorne team went out to begin raising their next round, in the midst of a tough economic climate. As PearX alums, we invited them to participate in our PearX S22 Demo Day, where Kai shared the latest happenings with thousands of investors in the Pear network. We’re so proud of the entire team for this next step in their journey.

PearX S22 Demo Day Presentation

I recently visited the new WindBorne HQ in Palo Alto, just a few weeks after the team moved in, and I left with a smile on my face. The offices were scrappy, the team was as determined as ever, and they were telling me all about the new advances with their product. I couldn’t help but look back and remember the first time they ever walked into my office as Stanford students and feel proud of how far they’ve come. I know this is just the beginning for WindBorne. We are so excited to continue to partner with them and to welcome Footwork and others to the team.

This past December, Pear VC was proud to invest in Infinimmune’s $12M seed round. Infinimmune is reinventing antibody drug discovery by focusing solely on human-derived antibody drugs and mining the insights uniquely gathered from deep characterization of the functional antibody repertoire.Here, we reflect on the broader field of antibody-based therapeutics and why we are excited about Infinimmune’s team, technical approach, and vision.

Antibody drugs have made an undeniable impact on modern medicine.

Since the FDA’s first approval of a therapeutic monoclonal antibody in 1986, more than 160 marketed antibody drugs have been developed to treat various ailments including cancer, autoimmune disease, infectious disease, and more.

Seven of the top 20 best-selling drugs of 2022 were antibodies, including Humira, Keytruda, and Dupixent. Collectively, antibody sales that year likely topped $200B, roughly on par with the sales of Apple’s iPhone.

Antibodies play a central defensive role in the adaptive immune system. Recent decades have witnessed tremendous, hard-won advances in the science of these amazing molecular machines and in their application as research tools, diagnostic reagents, and therapeutics.

Scientists have deciphered their molecular structures; decoded many of the intricate genetic and cellular processes that create and select functional antibodies; devised a variety of sophisticated approaches to identify novel antibodies that effectively bind a given antigen; and developed the tools and processes to reliably characterize, manufacture, and distribute them at scale.

Newer therapeutic modalities that rely on antibodies or components of them for their function, such as antibody-drug conjugates, targeted radioligand therapies, bispecific T cell engagers, and CAR-T cells, have become established drug classes in their own right. And in recent years, in silico design techniques, aided by ML/AI, have been used to engineer antibodies with better binding, stability, and expression.

Despite all of this progress, our state of understanding regarding the vast diversity of the antibody repertoire actually produced in humans remains shockingly low.

Limitations in the characterization techniques previously applied to this diversity, estimated at 10^11 to 10^18 unique protein sequences in humans, have stymied efforts to fully understand and gain insights from it. Even the advent of next-generation sequencing has not deeply impacted this space—most studies of the antibody repertoire still rely on bulk sequencing technologies, which only capture half of most of the variable region of one antibody transcript at a time.

Why does this matter in antibody drug discovery?

Because every day, inside every human, the body conducts the equivalent of 100 billion antibody clinical trials, testing each antibody for safety and efficacy in parallel. And these techniques have been developed and optimized over 500 million years of evolution of the adaptive immune system.

For instance, by studying the immune reactivity of blood samples donated from adults living in a malaria-endemic region, researchers were able to identify broadly reactive antibodies that exhibited non-canonical features (Tan et al., Nature 529:105-109, 2016). These antibodies were found to contain a large insert of an extracellular LAIR1 domain located between key antibody segments. This domain, which is non-canonical and which was not observed in narrowly reactive antibodies, increased binding to malaria-infected red blood cells. These results demonstrated a novel mechanism of antibody diversification that the human immune system can use to create therapeutically effective antibodies.

Clearly, human B cells produce antibodies that mouse B cells and humanized mouse B cells do not. However, the most common methods for discovering therapeutic antibodies today rely on screening antibodies produced in transgenic mice that have been immunized with the desired target antigen, or panning for binding to the antigen in relatively shallow pools of engineered human antibody-like binders expressed via phage or yeast display.

These approaches are not capable of leveraging the unique insights that can be captured by studying functional antibodies produced by the human immune system.

Enter Infinimmune.

Infinimmune is a startup that is reinventing antibody drug discovery by focusing solely on human-derived antibody drugs.

Infinimmune was founded by Wyatt McDonnell, David Jaffe, Katie Pfeiffer, Lance Hepler, and Mike Gibbons, a multidisciplinary team of scientists and technologists. These founders have deep expertise in immunology, genomics, computational biology, single cell sequencing, and data analysis, and they take a first principles approach to therapeutics platform development as drawn from previous experiences at 10x Genomics, Pacific Biosciences, and the Broad Institute.

As an example of this expertise, Wyatt, David, and Lance co-authored a paper in Nature last year that discovered a new property of functional antibodies coined light chain coherence (Jaffe et al., Nature 611:352-357, 2022). In this work, the authors used single-cell RNA sequencing to determine the paired heavy and light chain antibody sequences from 1.6 million B cells from four unrelated humans and incorporated a total of 2.2 million B cells from 30 humans.

They compared antibody sequences from pairs of B cells that were isolated from different donors and which shared similar heavy chain segments, specifically, the same heavy chain V gene, and the same amino acid sequence for a key antigen-binding region called CDRH3. [Note: an antibody is composed of a pair of one heavy chain and one light chain that are generated through a process of sequential gene recombination involving V, D (for heavy chains), J, and C segments.]

The authors found evidence of previously unrecognized determinism in the light chain segment (i.e. light chain V gene) used in functional antibodies, which were derived from memory B cells, as opposed to naive antibodies. The discovery of light chain coherence suggests that the sequence space for the light chain of a functional antibody, which has undergone selection by the human immune system to be useful, safe, and effective, is more restricted than what was previously believed. It also carries important implications for the design of therapeutic antibodies, transgenic platforms, and diversification strategies of antibody drugs.

With these types of capabilities and insights at hand, Infinimmune is developing an end-to-end platform to deliver antibody drugs derived directly from the human immune system.

These truly human antibodies are designed to drug new targets with improved safety and efficacy. Infinimmune is building its own pipeline of drug candidates while also aiming to partner with pharma companies to expand treatment options and reach more patients.

This past December, we were proud to co-invest alongside our friends at Playground Global, Civilization Ventures, and Axial in Infinimmune’s $12M seed round. We are delighted to work closely with the Infinimmune team, and we look forward to sharing many exciting updates to come. Infinimmune’s new HQ is in Alameda, and their team is always interested in hearing from smart, curious, and passionate scientists with a track record of innovation and building things from scratch. If you want to build better drugs for humans, from humans, you can reach the founders directly at founders@infinimmune.com or careers@infinimmune.com—there’s no better way to get in the hiring queue before more job postings go live in 2023!

10 years ago, we started what is now Pear VC under the name Pejman and Mar Ventures. But the story dates even further back to 2009, when Pejman approached me with the goal to build a fund that serves world class entrepreneurs and supports their efforts with know-how, network, and capital. Pejman had a clear vision to build a seed stage firm with a true legacy: one that would be talked about in the history books.

By that time, Pejman had established himself as a savvy angel investor, and he even backed some of my own startups. When setting out to start a fund, he wanted to partner with someone that had a complementary skillset: while Pejman had over ten years of experience investing, I had founded three companies. It was a great match, but I was initially pretty reluctant to dive into the world of venture. Pejman, like any great founder, did not give up. He spent four years trying to convince me, and ultimately the two of us agreed to set out and raise an initial seed fund in 2013. Raising our first fund was not easy. After all, neither of us had any venture experience and we did not fit the mold of typical VCs. After facing a series of no’s, a few brave LPs put their trust in us, and we were off to the races with a $50M seed fund.

Me and Pejman in Pear’s first office in Palo Alto in 2013.

So here we are, 10 years later. We are incredibly proud of how far we have come, but we’re also well aware of how much lies ahead of us. Over the last decade, we’ve seeded over 150 companies including marquee companies like DoorDash (NSDQ: DASH), Guardant Health (NSDQ:GH), Senti Bio (NSDQ: SNTI), Aurora Solar, Gusto, Branch, Affinity, Vanta, Viz.ai and many more.

Although we have come a long way since 2013, our DNA has not changed. Perseverance, can-do mentality, collaboration, service, and legacy remain the pillars of our fund.

The team has grown quite a bit. We now have a world class team of 26 (and growing!) Pear team members. Our investment team brings deep expertise across our vertical areas – from consumer to biotech to fintech to AI and beyond. We’ve also invested our resources in building a best-in-class platform team, with extensive backgrounds in company building – from talent to GTM to marketing and more.

Pear’s amazing team in our Menlo Park HQ.

Just like on day one of Pear, we are at the service of our founders. When we partner with a company, we are an extended member of their team and we do whatever it takes to help them be successful. We tell founders to think of us as “Ocean’s Eleven”: we’re a unique cast of colorful characters, with specific skills, a common plan, and coordinated execution. In fact, coordinated collaboration is at the heart of what we do.

We remain as optimistic as day one. Over the last decade of building Pear, we have witnessed the market go through its fair share of ups and downs. Despite the current economic downturn, we firmly believe that there is no better time to invest at the seed stage. The market is teeming with exceptional talent starting companies, the advent of AI is propelling company building at an unprecedented pace, and sales and marketing can be done at scale with fewer resources. In light of these factors, we are confident that the next wave of iconic companies will emerge from this downturn, and we are looking forward to being their initial backers.

This week, we celebrate raising our fourth fund at $432 million, but we know that fundraising is just one milestone. We have our eyes set on the decades that lie ahead, and we are already hard at work building new initiatives that will help us deliver on our promise to back and support early-stage companies.

Since day one, we’ve built Pear on this belief that people truly make the difference. We are deeply grateful to our LPs and to our founders who put their faith in us as partners every day.

We look forward to building the future of tech with Pear Fund IV. We couldn’t be more excited for the next decade of Pear!

A startup’s potential scale is bound by its future market size, and consequently “what is your market size?” is one of the determining questions that most VCs ask early stage entrepreneurs.

Estimate market size using a bottom-up approach not top-down. In other words, multiply the number of customers by the average revenue per customer per year (which you can estimate through multiplying transaction volume by price).

Present your total addressable market and your future revenue for 5+ years into the future.

At Pear we consider an entrepreneur’s clarity of thought and enduring ambition as more important than the market size number in a pitch deck. The objective of market sizing is to demonstrate that you are targeting a big market opportunity that you understand deeply. Startups have many unknowns and market sizing is a rough estimation, so keep it simple.

1. Why does market size matter?

Big companies can only exist in big markets.

Founder perspective: If you want to build a company that has a DoorDash-sized impact on the world then make sure to commit yourself to a sufficiently large market opportunity.

Investor perspective: If you want to raise capital from VCs then you need to convince them that your company will generate an exit value that returns their fund. In your pitch you should aim to convey that your startup has the potential to capture at least hundreds of millions of dollars of high-margin revenue within the next decade, within a multiple billion dollar market.

2. How to estimate market size?

Use the bottom-up approach to estimate market size. Multiply the number of customers by the average revenue per customer per year.

There are top-down and bottom-up approaches to estimating market size. The bottom-up approach is more convincing because its uses assumptions that are substantiated through other aspects of your pitch, such as customer definition, revenue model, and GTM. VCs also prefer bottom-up because the underlying assumptions can be tested and validated. Ideally you will only use top-down to sanity check the magnitude of your bottom-up estimate.

Keep your method simple and easy to explain. The underlying assumptions for market sizing will remain rough until you have ascertained your exact target customers and revenue model, so avoid undue complexity.

3. What is the exact definition of market size?

There is no single definition of market size. Early stage companies typically present three estimates for TAM / SAM / SOM. I encourage you to skip the acronyms and present bottom-up estimates for your total addressable market and your revenue in 5+ years.

We surveyed 30 VCs to better understand how other investors evaluate a startup’s potential scale. We learned that earlier stage investors tend to prefer market sizing presented as TAM / SAM / SOM, whereas later stage investors care more about recent revenue growth as well as estimates for future revenue.

Seed VCs generally value TAM estimates more because they have limited additional information to inform decisions. We heard from seed investors that: “TAM / SAM / SOM works fine as long as the methodology is clear.”

Series A VCs told us that they care more about future revenue even when looking at seed stage startups: “A bottom-up build of future revenue is more useful than basing SOM on a hypothetical % share of TAM or SAM.”

Growth-stage VCs pay less attention to market sizing and we heard that: “TAM is a crude indicator. Revenue growth is a better signal. It’s hard to grow 200% at scale if there’s a small TAM.”

The textbook definitions for TAM / SAM / SOM are vague.

You might have seen TAM / SAM / SOM in an article or a pitch deck. If you Google these acronyms and read a few articles then you’ll likely find varying fuzzy explanations (one example depicted below). Pitch decks often include a market sizing illustrated as three bold numbers within three concentric circles, without context or assumptions. Such minimalism saves one from committing to definitions that we might be unsure about, but it also forfeits this opportunity to present a compelling narrative that convinces investors.

Based on our survey of 30 VCs, it seems that many investors do not know the exact definitions either. So when presenting your market sizing, explicitly state your methodology rather than assume universal definitions. (These survey results also had me wondering whether later stage VCs are more honest about their knowledge gaps! )

The textbook estimation approach for TAM / SAM / SOM is

TOP DOWN ⚠️

Marketing textbooks generally describe the TAM / SAM / SOM approach as: first estimate your largest possible market for $ TAM, of which estimate a narrower proportion that fits your company for $ SAM, and then estimate the % market share you can reach to get to $ SOM. However, the % market share assumption is often an unsubstantiated afterthought, which results in a meaningless estimate for your company’s potential revenue. This approach encourages top-down thinking and is unconvincing.

The most consistent feedback in our VC survey was to dissuade founders from presenting their future revenue based on % market share of a large addressable market. So, what’s a better approach?

Present bottom-up estimates for your total addressable market and for your revenue in 5 years.

The market sizing definitions stated below are based on consensus across surveyed VCs. However, interpretation still varies so state your assumptions. Also, enough with the acronyms — replace the jargon with more meaningful descriptors.

Some of the surveyed VCs encouraged founders to drop the conceptual distinction between TAM and SAM. However, opinions on this topic were mixed. Instead of presenting both TAM and SAM, you could communicate your plan for incremental expansion across customer segments and products.

eg. Start with an initial wedge of selling product A into customer segment X. Then expand through cross-selling product B into the same customer segment X. Followed by expanding further through selling products A and B to a new customer segment Y.

4. When should market size be estimated for?

Estimate your market size for 5+ years into the future.

Surveyed VCs most commonly wanted to see market size estimates for 5 years into the future. If your company is many years away from IPO and/or riding a longterm industry trend (eg. transition to electric vehicles) then it’s more appropriate to estimate 7-10 years into the future.

A significant proportion of the VCs surveyed also prefer to see market size now as well as 5 years into the future. If you’re targeting a rapidly growing existing market then you can highlight that growth through presenting both now and in 5 years.

Guidance on the underlying assumptions

Now that you understand how to estimate your market size, you need to source the underlying assumptions to feed into the bottom-up equations. You can follow the following steps to arrive at assumptions for calculating total addressable market, initial addressable market, and future revenue.

1) # of Customers

1.1) Define your customers

Precisely focus on the customer segment that will contribute the majority of your potential revenue.

eg. While DoorDash could claim that every person in the US could potentially order food online, a more convincing segment might be: “Americans in the age range of 25-40, who are employed, and eat out at least once per week.”

If level of demand and/or willingness to pay varies significantly across your customer-base then you should capture such variation in your estimation through customer segmentation. Though keep it simple and only consider segments that will contribute significant revenue.

eg. Market sizing assumptions can differ significantly between SMB and Enterprise customers. If we’re selling a product into both then we should segment the market. (100K SMBs x 5 seats x $10K per seat = $5B) + (1K Enterprises x 100 seats x $20K per seat = $2B) = $7B total.

1.2) Estimate the total number of customers

The most relevant data sources vary by business category, eg.

Consumer: If you can define your target customer (or user) segment in terms of socio-demographics then use the US Census Bureau data on US Population.

Vertical-specific B2B: You can identify the number of relevant companies within an industry vertical using US Census Bureau data on US Companies.

Enterprise: If you your future revenue will be concentrated in big enterprise accounts then identify what proportion of companies within the Fortune100 or Fortune500 would buy for your product.

Additional example data sources:

Research reports (eg. Gartner, Forrester, McKinsey, BCG)

Government agencies (eg. Bureau of Labor Statistics, Bureau of Economic Analysis, US SBA, trade.gov, Bureau of Transportation, Dept of Housing, US Dept of Agriculture)

Industry bodies (eg. National Business Group on Health, National Restaurant Association, National Association of Realtors)

NGOs (eg. UN Dept of Economic & Social Affairs, UN World Tourism)

S-1s of companies in your category

1.3) Estimate the number of customers you could acquire in 5 years

You will acquire only a proportion of total customers We need to estimate a realistic number of customers captured by around the time you IPO, so 5-10 years from today. Its best to build this bottom-up through considering how many new customers you’ll be able to acquire (and retain) per year over the next 5-10 years.

Sense check your implied market share. Look at the market shares of existing dominant players in your category and in adjacent categories. Also consider strength of network effects, how entrenched established players are, and ease of distribution (eg. capturing 10% of the Fortune100 is more realistic than capturing 10% of 100,000 SMBs).

Our expectations for high market shares are often anchored in the dominant consumer-facing FAANGs, yet many other categories are more fragmented or under-penetrated. Pitch decks often state a 10% potential market share. Yet when tech companies IPO they have typically only attained a 0.1% to 2% share of their addressable market. See the chart below based on data in S-1s of recent tech IPOs.

2) $ Avg Revenue per Customer per Year

2.1) Select your revenue model

Identify the most relevant revenue model for your business. You might foresee multiple revenue streams, however its best to keep it simple and focus the market sizing on your core revenue stream. See the table below for examples (though this is not an exhaustive list).

Each revenue model is split into transaction volume multiplied by pricing.

2.2) Estimate Transaction Volume

This requires you to understand your target customer’s behavior. (eg. How many product will they consumer per year, How much data storage will they require, How many seats per company, etc.)

2.3) Estimate Pricing

Pricing is an artform worthy of volumes, and in practice you might chose to implement multi-tiered pricing differentiation to maximize your profits. But again, for estimating market size, minimize the complexity.

There are three main approaches to pricing. Value-based pricing is generally the best approach.

Value-based: Estimate how much value your customer attains from your product, and charge a proportion of that value. You can charge more through: (i) creating greater value for your customer; and/or (ii) heightening your customer’s perception of that value creation. Attribution is as important as the actual impact of your product. A rule as thumb is that you can charge in the range of 10-30% of the value you create for your customer.

Competitor-based: If your industry has pre-existing comparable products to yours then your customers are likely anchored in pre-existing price ranges. When pitching to VCs you might need to explain why your product has a premium or a discount to comparable products.

Cost-based: Estimate the cost to deliver your product and add a margin. Fixed costs are generally low in tech companies, and this is more relevant to operationally intensive and/or asset heavy companies.

How to best apply these approaches varies by the business category, eg.

B2B SaaS: Value-based pricing is the optimal approach to determine your customer willingness to pay. (eg. If your products increase your customer’s profits by $1M per year on a perpetual basis then you can charge a $100-300K per year subscription fee.)

Consumer: Anchoring to the price of adjacent products often informs the attainable price, unless your brand is highly differentiated. This also applies to consumer fintech. (See this article)

Healthcare: B2B healthcare solutions sold to payers or employers usually have a fee per member per month revenue model, and you can charge a proportion of the cost savings you deliver. D2C healthcare solutions usually a fee for service or a monthly subscription revenue model, and ideally you identify relevant reimbursement CPT codes. Healthcare also includes several more complex pricing models.

Marketplaces: The % take rate in a marketplace is driven by how much demand you can drive to your customer and how much easier you make it to run their business, as well as how competitive your market is. (See Lenny’s newsletter)

Now multiple those assumptions out. Hopefully you arrive at a big number for the addressable market. If not then revisit your assumptions as well as your overall vision.

Additional Tips

Think long-term and dream big. Most successful startups create or change markets, so you should estimate hypothetical demand for your product in 5-10 years, not just existing demand. Also consider how you will expand average revenue per customer through solving additional problems for your target customers.

Global market size is rarely relevant. If your strategy is US-focused then state an addressable market for the US only. If you’re starting in a smaller country and your strategy focuses on multiple similar countries then state an addressable market for those countries and be ready to explain your international go-top-market plan.

Ensure that the revenue you are presenting is annual. (eg. If there are 10M potential customers for your product and they might buy your product every two years on average, then you have 5M target customers per year.

For marketplaces, include take rate in the market size calculation rather than presenting overall GMV. For financial products, include fees rather than presenting total transaction value or AUM. If your B2B startup is helping your customer to increase their profits, then you can only charge a proportion of that impact.

Read S-1s of public companies with similar customers or products as your company. Search the SEC database for a public company of interest and open their ‘S-1 Prospectus’. S-1s are a goldmine of information and provide insights well beyond market sizing.

About Pear VC

Pear partners with entrepreneurs from day zero to build category-defining companies. Our team has founded eight companies and invested early in startups now worth over $80B, including DoorDash, Gusto, Aurora Solar, Branch, and Guardant Health. We use this knowledge to provide founders with hands-on support in product, growth, recruiting, and fundraising. If you’re building a category defining company then reach out to our team.

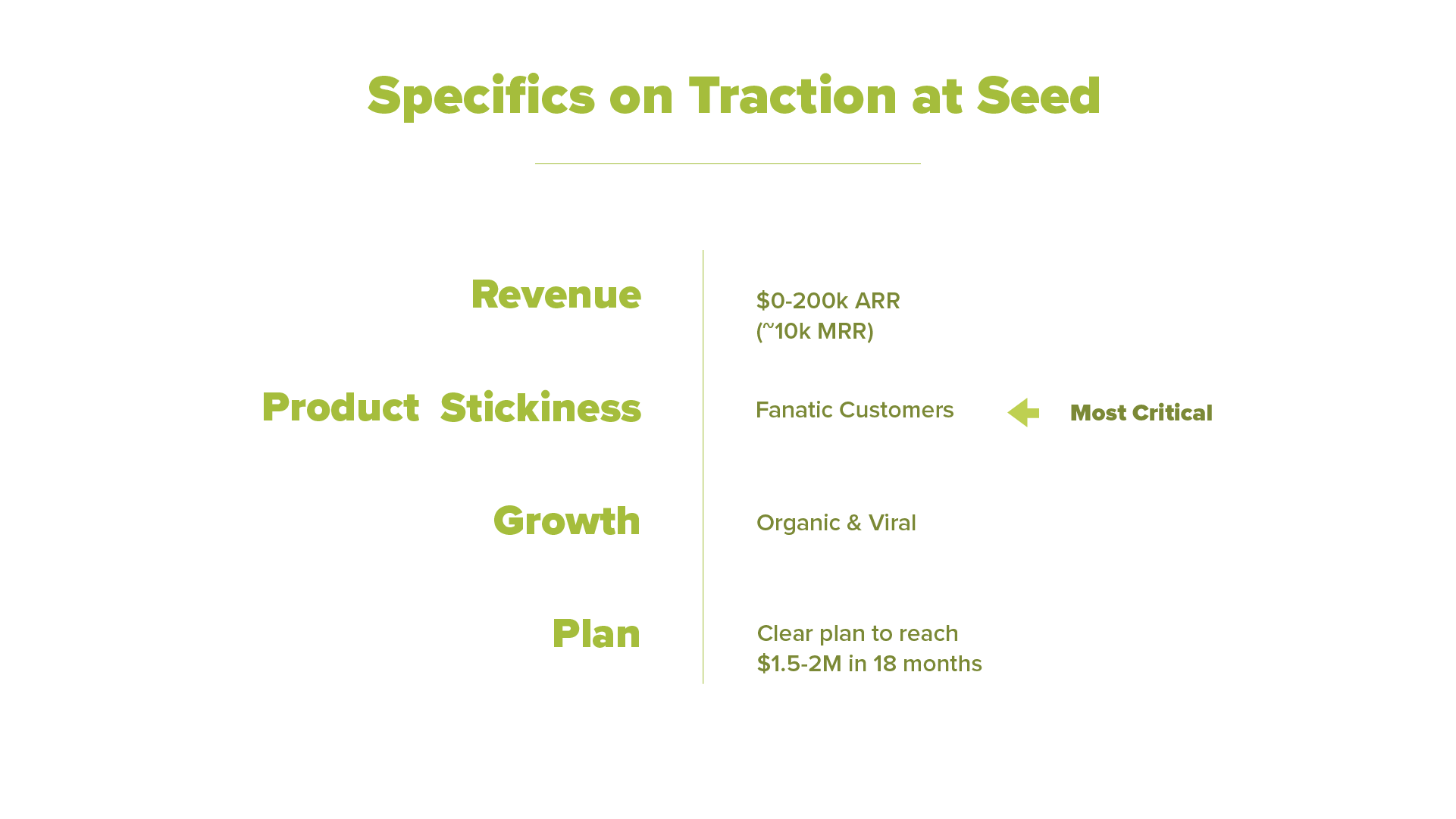

Let’s assume you’re a SaaS company that’s now raised some seed money. You’ve raised from us and you have two customers, and the founder has done all the sales.

Now your task is to prove two things:

someone who is not you can sell your product

you can optimize and scale that process

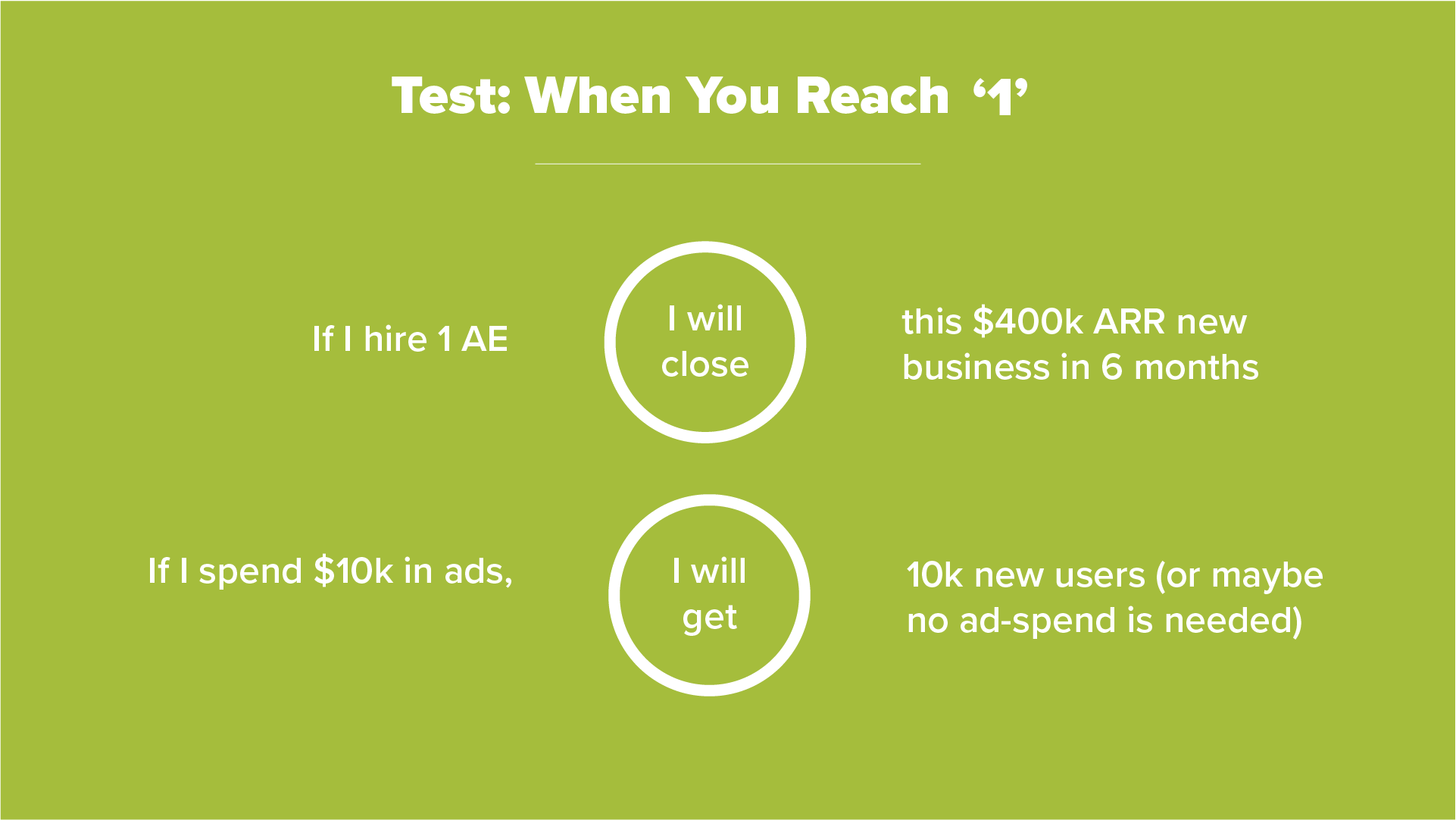

This usually involves building a sales team or setting up a reliable marketing channel. The test for this stage is whether you have a reliable formula for your growth. That is, you should be able to confidently say, “if I do X, I will get Y new customers / users / revenue.”

Pure growth is not enough. You can be growing super fast, but if you have no retention, we know that growth will die. Again, you may be tempted to buy a bunch of ads right before your raise to spike your growth for two months, but smart investors know that that’s not real growth.

You may be surprised to learn that pure revenue is also not enough. We have found that post-money valuation of series A companies and their monthly recurring revenue is not correlated at all:

If product love is the one thing that matters most to us at 0.5 stage, what is it for the 1 stage? That you’re going to be a “big company.” We are looking for predictors of success. You can think about it as the “second derivative” of your growth.

In this stage, we want to make sure that people not only love your product, but that they love it enough to pay you enough money to make it profitable to grow.

Even if you’re at only 200K in MRR, if we can see that you’ve gone from one person using your product to 20 people using your product, and those people are using you every day and they can’t live without you, you’re probably a great company, like Slack! They didn’t need to have 1 million in ARR for investors to know that people loved that product and that it was going to stick around.

Series A investors are going to look at your scale metrics, like LTV (lifetime value) to CAC (cost of customer acquisition).

To get to Series A from the seed stage (or from 0.5 to 1), the most important thing you need to do, as a seed founder, is to make a plan and measure your progress. Determine where you want to be in four quarters, then walk backwards and figure out what you need to achieve that.

Look at everything you need to do.

For example, if you want to be at $1 million ARR, with some amount of cash for six months at the end of Q4, you might determine that you need to hit $100K in revenue by Q2. You probably are also going to need enough leads by Q2. If this is a SaaS business, you may want to hire a salesperson for that. And if you have all these customers, you’ll likely want to support them and keep them happy, so you might have to hire a customer success person in Q3. To have something to sell in the first place to get to that Q2 revenue, you might need to have an MVP by the end of Q1 that requires hiring a certain amount of engineers.

You’ll need to do all this math to find out what that plan all costs and how much cash you need to have for it. It is likely you’ll need to iterate on this plan, which is why you also need to measure everything as you proceed. What gets measured gets done, and the bonus is that it’s easier to measure things at the seed stage! We love data driven CEO’s, and we even encourage founders to display their key metrics to everybody in their company. When you go out to raise our series A, you can just take your dashboard to the investors!

Once you have a plan, and you have your measurements, you’ll need to put those two together to figure out whether you’re on track or not. This sounds very simple, but we’ve had many founders suddenly call us with three months of cash left out of the blue. Force yourself to send reports to yourself, to your team and to your investors. When you do that, you’re actually committing to something, and that makes you true to the plan.

Here at Pear, we make every one of our seed companies run through a planning exercise at the very beginning of our partnership with them, and we review the plan every quarter. When our founders are in trouble, we review it every week, so we can figure out what our goals are and what we need to hit.

Final Stretch: Don’t Mess Up the Actual Fundraising

Fundraising is a little like selling a house. If you’re trying to sell a house, but you don’t have your inspections complete and you haven’t cleaned up the lawn, you’re probably going to get a lower final price than if you’d done all your work—even if you’ve got a great house!

Put another way: no matter how great your numbers look, you still need to have a great pitch. You have to actually communicate with data. You have to have a rational ask.

Remember, there are much fewer Series A funds out there than angels and seed funds, so the stakes are higher with each meeting, and it’s much slower and more complex. You can’t hand wave. You need to have concrete, quantitative answers, and investors are going to take several weeks to get back to you. It could take longer. The good ones do it fast, but it’s not 30 minutes.

Also, think through your process. Don’t contact 20 series A investors at once with your initial pitch. Stagger your pitches so you can iterate and revise between each, and save your top choice investors for last, after you’ve gotten feedback from the others.

This brings us to our final piece of advice for this process: diligence who you work with! We’ve seen founders get desperate and take money from investors they shouldn’t. We’ve done that personally on our own entrepreneurial journeys. It’s absolutely painful. You have to know who you’re fundraising from.

If you’re considering us as partners on this long journey, we hope you’ll take the time to get to know us, just as much as we promise to take the time to get to know you.

To review: at 0, you have a big idea. At 0.5, you have a product that you, as the founder, can sell, and you’re seeking seed stage financing.

What we’re looking for here is product love. For us, all that matters is — do people absolutely love this product? Is there a group of people out there who can’t live without this product?

Your product needs to be at least 10x better than anything out there, and ideally, you can show us that this group is willing to pay for it. To us, it doesn’t matter at this point exactly how much they’re willing to pay, and to some extent, even if they’re not willing, it could still be okay. We really want to see the love most of all.

Now, we do use some metrics and signals to try to determine that level of “love,” and it actually has nothing to do with how much revenue you have, nor acquisition.

Qualitatively, a good rule of thumb is that when a company is at 0.5 stage, they are no longer changing their website (or sales Powerpoint, or app) to acquire and retain a new customer. They’ve found a value proposition that works.

For a SaaS company, we generally want to see some very happy customers.

For a consumer company, it’s all about retention.

If you’re building an app, for example, you might be tempted to put your app out there and get as many downloads as possible. Maybe you’ll think about buying ads to juice those download numbers. To us, none of it matters unless you’re retaining the user. From our perspective, buying ads to inflate your downloads is just throwing money down the drain.

The top 10 apps, all of which are huge companies, retain their users at 60% after a year. The crappy ones retain under 10%. It goes to show that the hard part of a consumer app is to keep somebody using it for a long time. If you can do it, it’s a good sign that you’ve got that product love we’re looking for.

Another important signal we look at for consumer businesses is your retention of super fans—people who are dying for your product. A good example of this was Pinterest. Early on, Pinterest users were on the site all the time and they were obsessed.

So, we’re not just looking at retention of the average user, but also retention of those super fans. We want to see how much those super fans love you.

To navigate this stage, you’ll need a rapid experimentation mentality, cycling through as many new hypotheses as possible to land on the right value proposition. Make your operations scrappy and fast. Build and kill features, get to the simplest MVP possible.

To sum: be fast and listen to the data. Do not fall for fake signals. Remember the only real thing that matters is: do people (truly) love your product?